They also offer a checking account that pays 1.2% with zero fees and even waives ATM fees worldwide. These are all FDIC insured. I've been banking with them for about 6 months now and they're pretty awesome, outside of having a rather janky web and mobile app.

https://radiusbank.com/personal/high-yield-savings/

Radius High-Yield Savings is a free savings account with no monthly maintenance fee, no minimum balance requirement after $100.00 to open the account, and is FDIC-insured up to the maximum allowed. Annual Percentage Yield (APY) accurate as of 12/14/2018. Minimum amount to open account is $100.00. Rate tiers are as follows, 0.00% APY applies to balances of $0.01—$9.99, 0.05% APY applies to the entire balance on balances of $10.00—$2,499.99, 1.50% APY applies to the entire balance on balances of $2,500-$24,999.99, and 2.05% APY applies to the entire balance on balances of $25,000 or more. Rates may change after account is opened. Fees may reduce earnings.

$1,000 bonus on $150,000 deposit or more

$200 bonus on $10,000 - $149,999 deposit

Also, Citizens Access at 2.25% is also pretty good.

both of those are FDIC insured.

[0] https://blog.robinhood.com/news/2018/12/13/introducing-robin...

and interest rates are rising

Its the Theranos of finance!

it's now up to 2.4% for a online savings account, that is FDIC insured. i've been using them for 2 years now, and it's been awesome. As far as i know, 2.4% is the highest there is for online accounts. i'm surprised they don't top the list on nerdwallet.com

What I mean is, banks like Ally offer both near-highest interest rates, are well established, and provide a nice experience. Your savings account is bread and butter in your financial life. Using some "janky" bank just to squeeze few dollars probably isn't a good use of your time.

I'm not saying mysavingsdirect.com is "janky"; I really have no idea about them. But I've seen a number of higher interest bank accounts and turned them down because they were from unknown vendors.

As an example, I was pissed at Ally and needed a new vendor. I decided to try Discover Bank, figuring they'd be good with a well established reputation like Discover, and with the same interest rates as Ally. But the experience has been decidedly worse. Slower deposits and transfers, for example.

Also worth noting that usually you shouldn't be carrying a lot in savings anyway. Excess cash should be sitting in investments and doing work. So savings accounts will only be carrying emergency funds et al. If you've got, say, $12k in your account, an extra 0.4% is only going to give you a few extra bucks a year.

Is a few extra bucks worth working with a lesser bank?

Or, to the focus of the original article, is a few extra bucks worth working with an uninsured bank?

I advise extreme caution when it comes to savings accounts, which are explicitly for "safe" money in a health financial portfolio.

Slow deposits and transfers are not a problem at all. You only need to transfer in or out maybe a few times per year at the very most.

i'm not sure what you mean with "janky"

>> “I disagree with the statement that these funds are protected by SIPC,” Stephen Harbeck, president and chief executive officer of SIPC

As a result, I will not be signing up for Robinhood, that's for sure. I get the sense, It's not the place to park your money, if you're just trying to save up without investing.

we protect (money with a brokerage firm) that is used for the purchase of securities

or

we protect money with a (brokerage firm that is used for the purchase of securities)

Unfortunately, due to the nature of law, there's no way to get an answer on this until it goes to the courts which will only happen if/when there's a problem.

The only other story I can find on this quote right now is on CNBC. It's a little better. https://www.cnbc.com/2018/12/14/sipc-chief-raises-concerns-t...

NOTE: I do think these are important points to report, and important to understand if you are considering using the service. I will watch the development of the Robinhood checking with an eyebrow raised. I just really hate poor quality writing from 'top' news outlets. We should demand better.

What's "tech" about Uber or AirBnb?

mysavingsdirect has for the last 2 or 3 years shown they're commited to staying at the highest rates.

I consider software companies to be "tech" companies, but alas.

To answer your first question--if you go with Fidelity, they offer an "auto roll" feature which can re-purchase new T-Bills (or any Treasury/CD) at auction, automatically, when existing issues mature. It's completely hands-off: https://www.fidelity.com/fixed-income-bonds/fixed-income-too...

It would not be similarly notable for the National Enquirer to be caught making something up.

If Robinhood had offered this as a normal bank with FDIC insurance I would have been impressed. For now it just seems they're just moving a little bit higher up the risk/reward curve and trying to pretend the risk is the same.

FDIC insures the value of your deposits. SIPC covers the case where your broker or mutual fund cannot keep operating (eg. pay the help)

In a case like that all of your stocks and bonds are still there and have most of their value, but you can't get at them because there is nobody to process the transaction. Somehow the holdings need to be transferred to another brokerage or liquidated, and SIPC is there to make sure the resources exist for that happen.

Circa 1970 there was a crisis on "Wall Street" in the sense that many brokerages failed, see

https://en.wikipedia.org/wiki/Securities_Investor_Protection...

for a backgrounder on why we have the SIPC.

The danger that the FDIC protects us from is even more pernicious because fractional reserve banking is one of the most dangerous things people do. By design the assets and liabilities of a bank are very close to each other, in fact far larger than the equity of the bank. If the depositors want their money out, a bank might not be able to support the cash flow -- which means depositors REALLY want their money out.

The stock market on the other hand is "risky" because stocks can go up and down, but it is not dangerous systemically because if your stocks went down you have to accept that they went down. The bank is legally required to pay you back what you put in and promising to do that 100% of the time is a big promise. If people don't trust banks and banks don't trust each other then you can't cash your paycheck, get money out of the ATM, buy groceries, and then you really have a problem...

As I recall it, the 340,000 people of Iceland had no chance in hell of covering the enormous amounts even if they wanted to.

That's a very inaccurate recalling of history which you can see from reading the intro to the relevant Wikipedia article[1] and a summary of the EFTA Court's decision on the matter[2].

The case centered around a dispute between mainly Britain, The Netherlands and Iceland about how to interpret certain EFTA regulations. Iceland's position ultimately prevailed in court.

1. https://en.wikipedia.org/wiki/Icesave_dispute

2. https://en.wikipedia.org/wiki/EFTA_Surveillance_Authority_v_...

----

When Landsbanki was placed into receivership by the Icelandic Financial Supervisory Authority (FME), 343,306 retail depositors in the UK and Netherlands that held accounts in the "Icesave" branch of Landsbanki lost a total of €6.7bn of savings. Because no immediate repayment was expected by any Icelandic institutions, the Dutch and British national deposit guarantee schemes covered repayment up to the maximum limit for the national deposit guarantees – and the Dutch and British states covered the rest.[1]

The Icelandic state refused to take on this liability on behalf of the guarantee fund. Originally this was because the state lost funding access at credit markets due to the Icelandic financial crisis, but later proposed bilateral loan guarantees for repayment were rejected by Icelandic voters.

----

At the end of the day there were a ton of foreign depositors who felt like these were just normal savings accounts with higher rates, but when the financial crisis came they were in a much more difficult position than people who used domestic banks.

Many of the institutions I had CDs with were dissolved and I was refunded the principal (without interest) by the FDIC. Compared to the losses everyone else was seeing I was more than happy with my 0% "return".

Consumer savings accounts had absolutely nothing to do with the crisis.

Like, on the list of “things that caused the crisis,” they would literally be dead last.

Did you know your parents had savings accounts that delivered 10% interest at one time? Look up historical interest rates in the US. 4% is like average.

1: https://en.wikipedia.org/wiki/Federal_funds_rate#Historical_...

The consumer banking side of the story has almost nothing to do with it

https://investor.vanguard.com/etf/profile/VCSH

It is entirely possible for them to safely promise a 3% account under these conditions. This is not at all like the financial crisis. It's just wrapping an investment grade bond fund in a bank account interface.

Additionally, Robinhood is reportedly investing proceeds in US Treasuries. US Treasuries have a completely different risk profile than corporate investment grade bonds.

Ex: You buy a $100 bond at %3, then the prime rate goes up %1 so the typical market price of bonds of your class are now %4. Now your bond is worth less than $100 if you were to liquidate it.

Big difference.

It is precisely this kind of bundled 'derisked' derivatives which caused the last financial crisis (those were sold as very low risk mortgage debt , these are corporate debt).

The 3% return is compensation for the added risk. The financial markets are pretty efficient for liquid stuff like this.

Banks also provide services that consumers are willing pay for through lower rates on their checking accounts, and need to cover their administrative costs or have some other way of making money with the deposits.

A bond fund like that, even with a relatively short duration of 2.65, is going to have significant price movement in the principal amount due to interest rate risk. (Not counting credit risk etc -- credit spreads could move significantly too in a financial crisis.)

A big rate move coupled with a big jump in credit spreads could easily move the price of the underlying by several percent in a matter of days.

Not so cool when your deposit of $100 can only be cashed out for $97 a few days later.

If you want a guaranteed return you do not buy bonds or stocks. You buy a money market fund like VMMXX. See https://investor.vanguard.com/mutual-funds/profile/performan...

"There is a lot of confusion about what Robinhood’s thing is. Delightfully, it is called “Robinhood Checking & Savings,” apparently because calling it a “checking account” or a “savings account” would come too close to implying that it is a real bank account insured by the Federal Deposit Insurance Corp., while “checking & savings” is not a thing and so does not carry that implication. A magic ampersand!"

How the hell did this product get launched?

Fidelity Investments pioneered this product, and now it's available from others like Schwab.

But at Fidelity, the cash management account is distinct from the brokerage account. While the brokerage account is insured by the SIPC, cash management funds are swept into FDIC-insured balances at actual banks.

Looks like Robinhood is gonna lose on this one.

Source: https://www.fidelity.com/cash-management/faqs-cash-managemen...

The CMA account has mobile image deposit, free online bill pay, check writing (with free checks), free ACH transfers, free wire transfers, ATM/debit card (with ATM fee reimbursement at any ATM worldwide, no less), etc.

The only “best-in-class” factor that Robinhood has presented is setting the interest at 3%.

The somewhat recent addition of crypto is just depressing. They've integrated it with chat and live announcements of transactions, so you see people's names as they buy $1500 or $2500 worth of crypto as the whole market makes an inverted hockey stick nosedive to zero.

But the most absurd thing was seeing the HN comments yesterday as people were saying they were living up to their name of taking from the rich and giving to the poor. They're doing something worse--tricking non-rich people into thinking they'll get rich, while making a ton of money in the process.

I have been using Ameritrade for a while and was curious about their no fee platform so gave it a quick go. The graphs have no legends associated in the app. The spreads seems not up-to-date with official quotes, etc. I went back to Ameritrade as fast as possible.

They are the "go fast and break things" of finance. There is a good chance that this will not end well.

1) They knew SIPC wouldn't cover it, but decided to lie about it anyway

2) They weren't competent enough to assess the risk that SIPC wouldn't cover it, but decided to launch anyway without contacting the SIPC

Regardless of which is the truth, I wouldn't trust my money with someone who does either. Might as well jump into a tried-and-true pyramid scheme like bitcoin!

It might work, but in this case, the people most likely to get screwed are the customers.

Not sure that leaves a lot of room for speculation - don’t sign up to use Robinhood as a savings account unless you are comfortable doing so without an FDIC level of guaranteed protection.

Robinhood thinks their checking account should fall under the SIPC...so is their bank account not a bank account? What am I missing?

It's kinda smart - but i'm curious how they settle some of the backend with daily transactions moving in and out - if they're actually making bond purchases/sales with each transaction, for each customer each day, or for all customers each day etc.

edit: fwiw I think the entire premise of these new products and 3% paid (way over what treasury bonds pay) is as a loss leader to the gambling that is a lot of the "investing" done by Robinhood users. Must be temping to buy some Tesla options once you have a chequing account in the same app.

edit 2: their fine print:

> Robinhood Checking and Savings is an added feature to existing Robinhood accounts and is not a separate account or a bank account.

so they're saying they might market it as a bank account, but it isn't

The question then becomes whether this is a good kind of move-fast-and-break-things a la early Uber breaking into an over-regulated market, or if it's defeating an important protection that consumers need.

Money market accounts have been around a while. Is Robinhood's account different because they are subsidizing it to hit 3% APR?

ffs - they didn’t even do the most basic due diligence on this?

This is not just an indicator that this particular product might be in trouble, this is another order of magnitude kind of incompetence that makes me wonder why anyone would trust this company at all.

Wouldn’t you have to feel like the probability they end up with a major security issue, funding issue, executive behavior issue, etc., are all magnified by this knowledge?

I mean really, this is a staggering thing to read. I don’t think there could be hyperbole in this, it’s just incredible hubris-based incompetence.

[1] https://d2ue93q3u507c2.cloudfront.net/assets/robinhood/legal...

So it is insured, unless they can prove it's not for investing?

Think through this like a court case, where the insured is suing the insurer.

The insured doesn't simply go in front of a jury and state, "SIPC owes me $N. I rest my case."

consumer securities purchases protected by sipc

robinhood bank checking format:

deposit: money -> account -> robinhood backend securities purchased

withdrawal: robinhood backend securities sold -> account -> money

Is this the argument made by robinhood? Perhaps if that is laid out clearly in contract, i.e. robinhood is granted agent status to purchase and sale securities on behalf of consumer

Not exactly confidence-inspiring, but we will see.

It's just VC money being burnt to acquire more market share. The intent isn't to be profitable on the actual services provided, but to grow revenue and profit on an eventual IPO.

As an example, if I'm going to own my car anyway, I'm going to pay the time-based depreciation whether or not I drive Uber. My marginal cost to drive a mile is around 10 cents for power, 2 cents for tires/brakes, and 2-3 cents for miles-based diminution of value. The fact that GSA/IRS allows $0.545/mile doesn't mean that's my actual marginal cost, just that that's a permissible financial rate for profit-seeking business usage. (As one example, the IRS only allows $0.14/mile for charitable deduction driving, which squares pretty well with my marginal cost estimate above.)

Near as I can tell from a few minutes of Googling, Uber pays $1.35/mile and $0.21/minute in Boston, or roughly 10x the marginal cost of driving a mile. That leaves a lot of margin for driving to/from fares, positioning yourself to an in-demand area, disputed rides, Pool differences, etc.

A: Are our customers accounts insured?

B: Yes, through SIPC, which is like FDIC for brokerages.

A: Great! Let's create this product.

No more questions were asked.

You just don't launch a financial product of this nature, out of your ass like that. If that was the case then Robinhood customers have legitimate reasons to be concerned about the safety of their funds and securities. (For the record, I'm on of those Robinhood customers).

Of course, maybe that didn't happen, but between the idea that RH would build and announce a new product without running past the proper regulatory authorities, and the idea that the president of SIPC might just be wrong ... well, the latter seems more plausible to me.

Their website says "Robinhood Checking & Savings is launching early 2019."

Which may be the whole point of the offering.

Second, the SIPC boss probably is not in the best position to understand how RH is setting it up. Harbeck seemed unaware that the "cash" in RH accounts was actually going to reside in investments like Treasuries and thus be covered.

These accounts remind me a lot of the accounts offered by Washington Mutual right before there was no longer a Washington Mutual. Except back then, their bold rate offering was only something like 1.5%. A lot of young dumb people are going to lose their shirts on this one.

The only thing that has changed here is Robinhood is explicitly marketing their brokerage account as being able to be used as a savings account without any need to invest in securities.

It’s not black and white on either side. If there ever was a default event, it would surely go to court and it’s not 100% clear who would win. For that reason, I wouldn’t make use of the account.

Downvoters: you are confused. When you move cash to a brokerage account, it's protected by SIPC. It's a loophole, because this protection was not intended to be for permanent cash parking in an account - but there is nothing that can stop that protection from taking effect. SIPC statute is clear, cash in account is protected. You don't have to invest it, you just have to move it there with the intent of at some point maybe investing it, which is impossible to verify.

"“The statute that we administer says that we protect money with a brokerage firm that is used for the purchase of securities,” he added. “On Robinhood’s help page, it says that you don’t need to invest to use Robinhood checking and savings, that statement is wrong. If you deposit money for any other purpose, it is not protected.”

If they disagree it's a brokerage account, and it's certainly not being sold as such, then it seems to me there's alot he can do.

But that aside, here's the point you're missing: Robinhood is marketing this as a product that can be used independently of brokerage purposes. SIPC covers brokerage firms and, yes, cash in such accounts. But the SIPC president is arguing that it's not a brokerage account if it's marketed as an independent product for people with no intention of using it as such.

this sounds like a lot of silicon valley darlings

That sounds extremely profitable, so long as you stay ahead of the law - just like Robin Hood, in fact. But in this case it's not taking money from the rich ...

Such as?

They shouldn't be using Robinhood to buy individual stocks, buy cryptocurrency, or do options trading.

For me the strangest thing about their business is their zero-fee approach. Yes you can make money by getting interest from uninvested funds + premium subscriptions + trade arbitrage, but if it's such a good business why aren't the incumbents taking similar approaches?

Contrarians would say that incumbents are just to engrained in their past approaches to actually adopt modern strategies, but I had that extremely hard to believe, especially when one of the incumbents, E-Trade, was the pioneer of online trading.

Also, unlike other industries, financial firms are savage. They're not scared to make risky bets and spin-off new businesses and strategies. Their industry is naturally risky, so they have the experience and tenure to make risky bets, without souring stakeholders.

I always give Robinhood the benefit of the doubt, because in my day to day I personally can say that it works great. They definitely nailed the Customer Experience. However that doesn't mean that they have an actual viable long-term business, so I prefer to stay reasonably cautious... Time will tell.

They do, they just charge you extra commissions on top of what they make selling order flow, etc, etc. Commissions make up a miniscule portion of income for brokerages. I think that fees a) keep out the "riffraff" and b) brokerages know that it's a zero-sum game to compete on them.

Asking this question is like asking why Ally and Goldman Sachs can offer 2% APY savings accounts, but Bank of America and Chase can only offer 0.01% APY.

There are similarly low-cost brokerages which offer dangerous products, like $500 intraday futures margin (about 250x leverage), 400:1 leverage on Forex products, or more traditional low-cost stock trades. The difference between $5/trade, $1/trade, and $0/trade isn't that significant in reality.

[0] https://www.forbes.com/sites/melaniehaiken/2014/06/12/more-t...

I agree though that Robinhood is a different story with potentially harmful consequences for unsophisticated investors looking for a safe/easy investment.

These companies are not democratizing investment, accommodation, tranportation or whatever they are rent seekers that use a combination of technology, business model and rule breaking to extract a portion of every transaction.

They explicitly position themselves as 3rd party to the transaction. While the rest of us suckers play by the rules or gasp work to change them, they realize a portion of their advantage by just ignoring them.

And for its shareholders, so is a factory dumping heavy metals to the nearby river. And for its customers, so is a slave plantation.

You judge businesses by the treatment of all participants of an economic activity, not just the ones giving and receiving money. Uber and AirBnB are examples of companies that shit on society at large to provide better service to some small fraction of it. In a civilized world, there's no place for this, which is why it saddens me deeply that they're still around.

EDIT: The fact that these crimes "have happened at hotels/in taxis as well" ignores the fact that they are far more likely in an environment where regulations meant to prevent or reduce them are wholesale ignored.

Uber and AirBnB both flouted primarily city-level regulations that are tough to enforce against external players, and where they broke larger rules it was by pushing vulnerability onto their service providers (e.g. drivers who assume Uber handles taxes like they're direct employees). And at least some of the regulations they ignored were so obviously protectionist that "look, we're breaking the law!" could actually form a selling point. (Which let them redirect focus from more popular rules like property hygiene.)

Robinhood is tangling with national financial regulations, which for all their loopholes and weaknesses are made to take on far larger players with a history of bad behavior. Meanwhile, the rules they're breaking are pretty much all directly tied to consumer protection, so it's going to be mighty hard to run an ad campaign to raise sympathy.

It reminds me a bit of Theranos, actually - "fake it till you make it" wasn't novel, but they neglected massive differences like offering an unsustainable service versus signing unfulfillable contracts, or failing random website visitors versus crossing major corporations and the DoD. It's like a clumsy new lobbyist offering a bribe instead of making a campaign contribution and expecting consideration; the dynamics might be similar, but the gap in execution could easily destroy them.

That sounds like unilateral action, whereas what happened was that there was a dispute about how deposit guarantees should be treated within the EFTA agreement, and all parties involved ultimately didn't insist on what they individually felt like doing, but followed the rulings of the EFTA Court.

But yes, it was a big learning experience for everyone involved. But that's exactly the reason it's important to make the distinction.

It's not that Iceland was unilaterally callous and pursuing those relatively small amounts was deemed small potatoes. Rather, EFTA rules were clarified in a way that would also apply to e.g. French depositors in Danish banks should a similar Danish default occur in the future.

What happened with domestic depositors is that the Icelandic state was free to selectively grant benefits to whomever it pleased once it became clear that its banks weren't subject to the EFTA deposit guarantees for anyone.

That's also an important distinction, and is why the action didn't violate the rules of the trade area.

No bueno.

… not without prominently mentioning the block chain, at least.

Unless they worked with the SIPC up-front to ensure that these funds would be covered, and that the SIPC actually, you know, has the means to cover them, then the only way account holders are going to find out if their are protected or not is in the aftermath of a crisis, after a long and drawn out lawsuit.

When I saw the headline, I thought about signing up but hadn't gotten around to reading the fine print.

Glad I didn't waste my time.

The new thing here I think is the ATM card and them covering the difference between the money market rate and 3%, which right now is less than 1%. They'll probably make up that difference via interchange fees when you use the debit card.

That SIPC thing though ... that's a bit of a wrench in the gears.

Even if they don't actually achieve the 3% APR checking accounts available ("sorry, it's actually 2% like the rest"), they still got people to sign up and they won't not register because they'll convince themselves "oh I got a debit card, and brokerage account, etc etc...who cares this is still great")

#growthhacking

Though hanlon's razor makes me think this was more them not thinking things all the way through than a devious plan to get a bunch of signups without ever launching anything.

(ok, unless you count the US crap list such as BoA, etc)

Incidentally, here is a really good article about what happens when the FDIC takes over a bank:

https://www.npr.org/templates/story/story.php?storyId=102384...

My understanding is that:

- "Cash" in brokerage accounts is usually actually some form of investment, and is usually listed as such (eg, as a deposit, money market fund, etc). The SIPC protects the holding of the investment, not the value of the investment, so if the fund goes bad, there is no protection.

- Cash in brokerage accounts is cash, and is not very common. It isn't going to make any interest, because it's not being invested by either the account holder or the brokerage, unlike fractional reserve banking. The SIPC protects this, but that's because it shouldn't have been at risk anyway.

The Robinhood account is thus confusing. If it is offering interest, then it's not cash, but a cash investment, and the actual value of the investment, which is what the clients would actually care about, isn't protected at all.

Edit: it appears they've pulled the announcement. Reading into that apology, maybe it was some sort of sweep into FDIC-insured bank accounts? But if so, how could that possibly offer 3% return?

edit: a better way to explain it - we'll give you tbills at 3% p.a and let you pull out/in whenever you want and handle the rest is a hell of a business model without the rest of the story

In addition, I'm guessing their AUM are low relative to their popularity. Lots of millennials may be very vocal about Robinhood, but may not have the quietly massive asset balance that boomers have, tucked away in Schwab, Fidelity, or Vanguard. This could be a land grab for AUM to support future VC rounds, an acquisition, or an IPO.

Currently the world in general is very far from an economic boom, and central banks are actually implementing desperate monetary policies to jump start inflation. Thus, we are very far from those times to the point that nowadays a 3% interest rate is considered huge, as the norm is for interest rates to remain below the inflation rate

When you account for the investor cash that will subsidize this service as a loss leader offering, it’s not unreasonable.

The only risk is we enter a severe recession and the fed has to drop interest rates to 0 again. In that scenario, robinhood simply has to lower the rate of their offering as well. This isn’t some big existential risk.

That's just not true. A significant contributor to the mortgage crisis is that banks loan out savings that are backed by the government. Savers deposit their money with banks even if those banks are underwriting risky mortgages

Not sure I follow your argument. How did savings accounts that offered 4% cause the crisis?

Over the last 12 months, the price of the VCSH fund is down more than 2%. This offsets the dividends paid with the coupons received and results in flat performance.

[1] https://www.accessdata.fda.gov/scripts/cdrh/cfdocs/cfcfr/CFR...

Ingredients: Mechanically Separated Chicken, Beef Tripe, Partially Defatted Cooked Beef Fatty Tissue, Beef Hearts, Water, Partially Defatted Cooked Pork Fatty Tissue, Salt. Less than 2 percent: Mustard, Natural Flavorings, Dried Garlic, Dextrose, Sodium Erythorbate, Sodium Nitrite

Still not a panacea, course. What was the ROI on the S&P 500 between, say, 1997 and 2009? Ouch. We've been on a beautiful bull run for the last decade, at least up until a month or so ago. I wonder what the next decade or two will look like.

I started at £120 a month and it was ten years before I started now my minimum buy is £2000 and I only do the occasional single stock even now 20+ years later.

There are also costs per position per investor. Some services that brokerages have are based on position counts. An investor with 10 shares in 1 stock is cheaper to maintain than an investor with 1 share in 10 stocks.

(One example is prospectuses. If you buy a fund, you're entitled to the prospectus to be delivered within a certain amount of time post trade. If you just by 1, 2, 3, then 4 shares of the same fund, you only get one file/document delivered to you.)

If I'm a fisherman in Florida, and I need to follow regulations for the fishing industry there, they don't have a stipulation that you can't discriminate against certain persons based on age, raced, gender, etc. when you take customers out on expeditions.

Why? Because that's covered by United States law.

Yes these things happened, and yes they are atrocious but they have nothing to do with the regulatory gray areas that these companies operated in.

With a centralized platform, people selling rides or lodging actually get recorded when they reject people, which makes it possible to pursue them for discrimination.

- Uber/AirBnB's regulatory abitrage

- assault, harassment, or illegal discrimination

but this is a complete non-sequitur. The laws that they're avoiding have nothing to do with individuals hurting other individuals. And assault, harassment, or illegal discrimination are perfectly possible in the context of a licensed hotel or taxi.

Simply put, Robinhood has far more at risk than the SIPC by launching without SIPC insurance. The banking industry is heavily regulated and Robinhood has been in the brokerage game for enough now to know that a major product launch like this in a tightly regulated area requires massive amounts of paperwork and approval. A mistake like this could collapse not only this new product but also their brokerage. It's far more likely that they have done their due diligence before announcing and launching a product that has that big of a risk.

Edit: We don't even have to wait! SMH...

https://www.google.com/amp/s/techcrunch.com/2018/12/14/robin...

https://www.cnn.com/2018/11/02/tech/uber-self-driving-tests/...

To be fair, they're proposing significantly improved safety procedures. To also be fair, there are not many people (as opposed to corporations) who would be out on good behavior 6 months after being convicted of vehicular manslaughter.

Unless one doesn't want to notice, that is.

SIPC on the other hand is more relaxed because it covers less. It only covers when a member broker becomes insolvent and is unable to return a security to you that you own.

There are similar funds that invest in short term treasuries and often that you can write checks against, however they don't offer 3% and they're very transparent that you own these securities and are subject to the (very low) risk that comes with owning them.

Robinhood's marketing sounds a lot more like a standard FDIC insured bank account but they're saying it's SIPC insured instead, and the SIPC is confused about what securities they would actually be insuring

However, in this case, won't it be more like a bond-fund, where the fund essentially has a ladder of bonds that are constantly expiring and getting reinvested (and also investing new investments from retail investors), and so the overall value of the fund may still remain close to $100.

I could well be wrong, so please feel free to correct me! Trying to learn.

If they called this the 'bond fund account' with easy liquidation and buying to make it bank account-ish, then I don't think people would be as upset about this, but it would be a fairly niche financial product.

What people seem to be misunderstanding is that a yield curve exists. If they were to go the safe route of short maturities, the interest rates will be must lower than long dated securities. If they reach for yield in longer term securities, they will have to mark to market when interest rates rise (which they most likely will due to the fed signaling that they'll be tightening in 2019).

You can't have your cake and eat it too

Why not? Shouldn't Icelandic law protect Icelandic residents?

So it’s good to protect Icelandic residents. But the law is inefficient if it allows too much capital that it can’t be managed and insured.

> it’s illegal to murder someone regardless of the perpetrator or victim’s nationality

You're mixing up two things: whether the law as it exists was violated (in which case Icesave should of course be punished) and whether the law SHOULD protect foreign depositors. I'm discussing the latter.

> bank insurance applies regardless of nationality

I'm not well-versed in cross-border banking to say the least, but isn't that an opinion? One could just as well argue that Icelandic taxpayers shouldn't have to subsidise the British (as an example) public, by providing free insurance. If Britishers want insurance, it's up to their government to incur the costs, since it's the Britishers who'll be benefiting.

This isn't to say you can't make money as an individual by day trading, but it is to say that the median day trader would have made more money by buying an index fund and sitting on it for a decade.

Stock trades aren't instantaneous, and they're not guaranteed to resolve in the order they were submitted. Wealthy traders can throw money at a combination of locating their servers physically closer to the exchanges and just straight up purchasing preferential treatment from them in order to ensure that their trades will always resolve ahead of yours. Moreover, the "price" of a stock is essentially the rolling average of all the buy and sell offers currently in open. When you "buy" a stock from Robin Hood, what you're actually doing is creating an offer to purchase at or below a specified price point.

One of Robin Hood's main sources of revenue is providing access to that stream of trade offers to investment firms who can use it to "predict the future" in ways that will systematically erode your profit margins. There are any number of ways this happens, but probably the easiest one to understand is that after they see you place a buy offer they can use their position near the front of the queue to accept the cheapest available sell offers ahead of you and immediately resell them to you at your offered price, pocketing the difference.

That's the catch with normal humans trying to play the stock market. You can't actually participate in the same way that wealthy institutional investors do, because you can't afford to pay to be near the front of the queue. In fact, the way you participate essentially guarantees that, no matter how well you do, the institutional investors will be able to do slightly better.

One way to work around this is for normal humans to pool their resources so that they can collectively act as a wealthy institutional investor too. That's essentially what index funds are.

If all RobinHood users followed sound "buy diversified ETF and hold" investing advice, my understanding is that they'd go bankrupt.

If Robinhood is incentivizing or encouraging frequent trading by users, that's not really good in my opinion. It doesn't make them worse than other brokerages, but it doesn't make them better either. And with a name like Robinhood, they are positioning themselves as white knights.

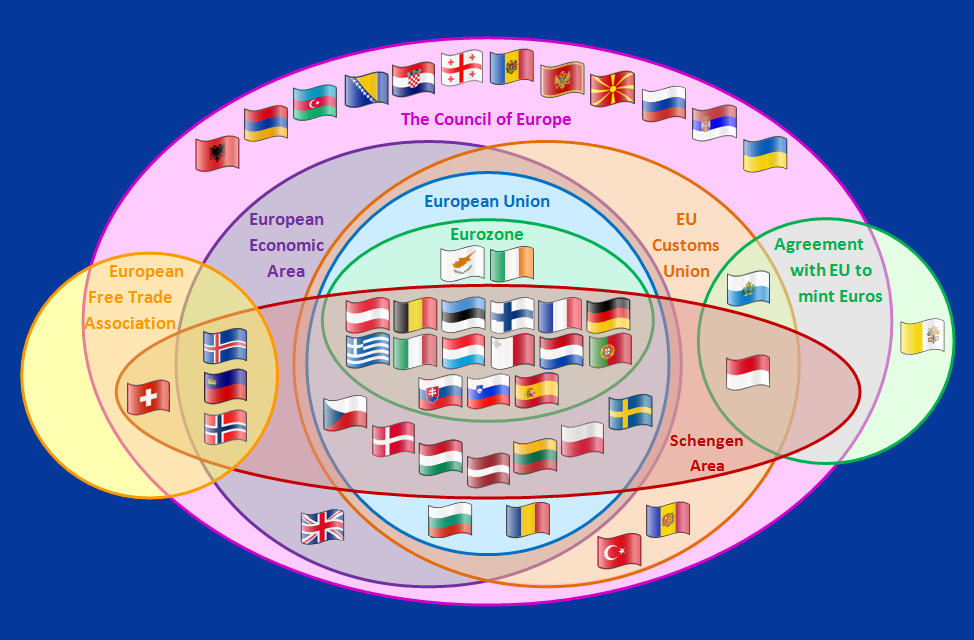

They once applied for membership after the financial crisis but it didn't go through; currently most citizens are opposed to the idea.

Becoming a full EU member would require them to accept the EU's fishing limitations, potentially hurting their economy. There are also other factors involved:

https://en.wikipedia.org/wiki/Iceland%E2%80%93European_Union...

[0] https://www.investopedia.com/terms/b/breaking-the-buck.asp

Literally all money market accounts are bond funds under the hood, actually.

Bond funds, however, frequently can and do lose value - if interest goes up, price goes down (the reverse should also be true, though).

If I sock away $100 a month for the next 12 months to pay for something, which one is more likely to have >=$1200?

Regardless of its legal structure, I meant "megacorp" in the generic sense of "large company."

It is a large company.

Vanguard has a pretty good reputation regardless of it's company structure. I'm not so trusting of some other financial firms.

Yes, you are. You're trying to freeze your neighborhood in amber, which is most definitely a sign of an inefficient incumbent.

Also, let's not pretend that AirBnB is progress. It's just a third party that encourages people to start illegal hotels, to earn money for themselves at the expense of their neighbours. This is not a case of local owners having opposing interests to society at large; this is a case of a company enabling some people to parasite on the others.

The incumbents I was referring to are clearly hotels and taxis. But I think it's also important to point out that I wouldn't presume to tell you who to rent to or for what duration since you own the home and it's your property. AirBnB is merely a facilitator of that transaction.

If you don't own the property, that's different story.

Sure, but you're forgetting about another party in the transaction: everyone else. You don't have to remember about them most of the time, because unlike Uber and AirBnB, most businesses aren't dumping externalities on non-customers.

> I think it's also important to point out that I wouldn't presume to tell you who to rent to or for what duration since you own the home and it's your property. AirBnB is merely a facilitator of that transaction.

That works well if you're the only one with a property within shouting range. Most people live (and most AirBnB activity happens) in large, organized groups. In a civilized society, you're not free to do anything you like without regard to the freedoms of others.

We live in a time/place where money is reasonably readily available; You take that away and "society" makes all sorts of accommodations for "you're preventing homelessness" and "you're doing what you have to do to pay your debts". Though given rising inequality, we might be closer than we think.

Probably other changes too.

but for real, country names would be helpful too

If I had browser data from everyone on RobinHood, and was able to track which stocks they were looking at, I might be able to make money front-running.

What if they do it for fun?

Personally, I would have fun having a few thousands there (but I'm Canadian), it's not worse than having a few thousands over a gaming computer, or gambling at the casino.

If you consider Robinhood as the way to finance your retirement, well you are doing something pretty bad, but that was always true for any stock trading.

> Investing, Checking & Savings. All for Free.

> Robinhood gives you the tools you need to grow your savings, invest in your future, and do more with your money.

Does that sound like "this is not an appropriate way to finance your retirement" to you?

All brokerage accounts advertise themselves as investments, even if the reality is that idiots open them and lose all of their money trading options.

I mean, if you really have this expectation of marketing copy, I don't blame you, that's a totally legitimate position to hold. It's just not one I would expect many people to share.

Robinhood presents a nice way of making it easy to get into the stock market with a pretty interface and without going through a cumbersome broker and paying fees for things you don't understand. Do seek professional help if you are looking for 401k and retirement guidance.

If anything, RH is sophisticated gambling.

But people like me should recognize that the people using Robinhood to trade individual stocks, buy cryptocurrency, trade options or trade on margin are effectively subsidizing those who do. Along with the participants of Robinhood's funding rounds, I guess.

The only real reason to have money in RH, IMO, is if you're gambling with <$1000 on penny stocks and options-cum-lottery tickets.

And yes, this criticism does apply to most brokerage accounts. Most brokerage accounts don't have half of Silicon Valley fawning over them, though.

I'm not a Robinhood user, but I use simple.com as a bank. It's like every other bank in that it holds money. If anything it's somewhat less convenient than banks with physical branches. But the online UX is so vastly superior to every other bank I've used (large sample size) that I'm a rabid fan.

[Anecdotally, someone on r/tradexiv or r/tradevol or somewhere on Reddit had a post about their Vanguard advisor cautioning them about buying XIV earlier in the year, telling them, more or less, "you're either exposing yourself to a lot of risk, or you're too smart to be trading with Vanguard" ...... he was not, it turned out, too smart.]

My claim was that RH should not be where you have money that you use for long-term buy-and-hold investment, even outside of an IRA. I think using RH for speculative investment is fine(-ish) if you accept that their order execution is poor (you don't really see this until you get into options), the company has severe product issues (e.g. the options order error the other day causing them to halt all options trading), and the company is not very well established (so there is a non-zero, greater than average, default risk).

I think it's undeniable that RH's UI is prettier than most other brokers. However, I think it's obvious that "prettier" and "better" are not necessarily the same thing. Again, if you are a buy-and-hold investor (which, again, is what I was responding to), being able to make a quick trade is not important, since you should probably only rebalance your portfolio once a quarter (maybe monthly or biannually, depending on your level of engagement).

But specifically, RH's UI is deliberately minimalistic, to a degree that I think is starting to verge on dangerous. They only recently moved from spark lines to offering optional OHLC bars, and their charts have no axes, which makes it difficult to get a sense of the products price movements. RH doesn't show you historical OHLC data, or historical dividends (just yield). The app offers no stock screening. The charts offer no volume analysis, which makes it difficult to see whether or not you'll be able to exit a position. My mom (who thankfully understands that she should only put money she's willing to lose into RH) recently told me she entered into a position with some low-volume real estate company, and couldn't exit the position for some days due to lack of buyers. She was unaware of the liquidity of the product she was trading (and complained that RH should have warned her... but that's another story).

Even worse is their options platform. At minimum, it's useful to show the days-to-expiration when selecting the expiration date. The options platform deliberately hides important information, such as implied volatility (probably the most important figure for an options contract), Black-Scholes greeks, volume and open interest, and a probability of profit estimate, behind an unlabeled corner button after you've selected an option to purchase. RH introduced multi-leg orders over the summer, but these still don't really give you the tools you need to construct strategies like spreads, calendars, straddles, strangles, condors, and butterflies. These are fairly complex trades with non-linear responses to spot and volatility changes, but RH won't even show you your net position delta before placing a trade (it will show it to you after you've entered a position). If you want to see what a real options trading platform looks like, you can demo ThinkorSwim or Tastyworks. Yes, it's more complicated, but that's because it's necessary.

So no, I disagree with the claim that RH's UI is "100x better". I think it's UI is maybe "50x prettier", but I don't think it's "better" for the user (and I've seen some wretched UIs, like Ameritas). In options trading, I think that RH's interface is objectively worse than those offered by other platform. Unlike checking and savings, which are generally regarded as low-risk activities, I think that RH's UI is deliberately designed to encourage risky behavior, and minimize "information overload" (in favor of "blissful ignorance") in what is inherently a risky activity for which most customers are not adequately prepared, under the thin guise of "democratization" (hence its beeline from stock investing (risky) to stock investing on margin (riskier) to cryptocurrency meme investing (extremely risky, and launched during peak bubble) to options trading (extinction-level-event risky for novices)).

Specifically, I have a boring investment strategy of SP500 and AGG. I'm just seeking the lowest cost means of investing in those two indices. When I opened the brokerage account RH was mostly top of mind. Things have gotten more competitive lately, with Fidelity's 0 expense ratio funds and maybe I should look at Vanguard more carefully. Although 'Vanguard is more established' isn't particularly resonant personally, so to my mind they seem relatively equivalent.

I completely recognize that RH's platform enables a lot of unsophisticated traders to make unwise trades, and leaves sophisticated traders wanting.

The extent of my knowledge just comes from reading /r/wallstreetbets for entertainment, while doing passive index fund investing for personal finance.

I think the best resource for anyone starting out investing would be "A Random Walk Down Wall Street" (Burton Malkiel), and maybe "The Intelligent Investor" (Benjamin Graham), even if you don't intend to be a traditional value investor. I think these books (I'll admit I haven't read all of The Intelligent Investor) set your expectations. I also listen to Masters in Business, Odd Lots, and P&L podcasts by Bloomberg (P&L is more short-term, while MiB and Odd Lots are more generally applicable). Both of those books might be floating around the internet.

I also really enjoyed "The Physics of Wall Street" (James Weatherfall). It's a look into how financial mathematics got started and how it has grown and been increasingly applied in modern finance.

If you're interested in options and other derivatives (I find derivatives to be the most interesting, and least arbitrary, financial product), I'd start with John Hull's "Options, Futures, and Other Derivatives", which is a textbook at maybe the sophomore or junior level. I hear the PDF is freely circulated online. I think understanding how options and futures work is essential for understanding finance. A slightly more technical text, "Dynamic Hedging" (Nassim Nicholas Taleb) is also good (and maybe also available online somewhere...). It is less philosophical and polemic than his other books, but doesn't resist calling you an idiot either, as is Taleb's style.

You might also find work on non-ergodicity (Ole Peters), the Kelly criterion, universal portfolios (Thomas Cover, 1991), and Ed Thorpe (a mathematician who derived a precursor to the famous Black-Scholes model) of interest (Ed Thorpe is an incredibly interesting person in his own right). If you find yourself wanting to get into technical analysis, I'd recommend "Evidence-Based Technical Analysis" by David Arons (a spoiler: the evidence is not good). If you're interested in ML applied to trading, I keep seeing references to Advances in Financial Machine Learning (Marcos Lopez de Prado), although I haven't actually read it.

Regarding other financial products, CME has a large number of resources available for understanding futures trading, although futures are generally too high value for regular traders to use safely (the highly liquid /ES contract controls ~$130,000 exposed to the S&P500 and allows one to take about 22x margin, or even as high as 250x for intraday trading). Similarly, there are some nice introductions to the forex market, but again I'd caution you to stay away. And as much as I'd similarly caution you about blindly following their advice (and in general about being a "volatility seller"[1,2] -- see Taleb's book), TastyTrade produces a ton of videos on options trading (particularly retail options trading), which include the mechanics of options trading and how their trading platform works (which is similar to TD's platform -- the CEO/Founder, Sosnoff, was involved in the development of it when he was at TD). You can download TD's ThinkorSwim and paper trade options, or just "preview" their application with delayed prices and see how options work.

Finally, rather than r/wallstreetbets (which is now 99% low quality memes and loss porn), I'd recommend checking out r/options and r/thewallstreet, which are more professional forums, and potentially forums such as EliteTrader and Nuclear Phynance as well.

[0] https://www.bloomberg.com/news/audio/2018-12-07/why-part-of-...

[1] https://www.bloomberg.com/news/articles/2018-11-29/broker-se...

[2] https://www.bloomberg.com/news/articles/2018-02-06/credit-su...

{kind=link}