Algorithmic stablecoins are provably impossible without continuous funding(fragileequilibrium.substack.com) |

Algorithmic stablecoins are provably impossible without continuous funding(fragileequilibrium.substack.com) |

To buy a loaf of bread, the price needs to pay for the wheat, ovens, energy and the employee costs. This relationship is recursion. The staff of the bread company need to afford bread of their own and shelter and energy and transportation.

Everyone is thereby supporting themselves and everyone else with what they purchase. This guarantees poverty as not everyone can scale their earnings to provide for themselves and everyone else as the prices all come from the same money supply. Inflation is baked in. This is why central banks don't want wage growth. If you understand recursion and recursive relationships then you understand that poverty is baked into the system. (Edit: due to not everyone producing more than they cost)

Think what this means for people at the bottom and give to the poor.

This isn't to say that charitable giving is bad. If you are financially stable and have money to spare, please donate your time or money to those that need it. It just isn't the solution to a national problem.

SF spends ~60k per homeless person per year (maybe more now). It’s clearly not money that is the limiting factor here.

Tax more and people do less as it doesn't pay to do more labour and get less of it back.

When people start a business they must borrow money and usually pay interest. That interest forces you to be profitable, you can't just run your company at 0% profit as that would only pay for your salary and the salary of your employees and the materials and machines you bought.

It is impossible for every company to be simultaneously be profitable. After all, if there is a million dollars in the economy, you can't have a 5% profit and reinvest the money as that would require a money supply of 1.05 million dollars. Thus, the money supply must grow endlessly and if the economy can't keep, there must be inflation.

I am one person out of 7 billion. I need to provide for myself, everything I pay must cover the costs of all the costs of those people I bought from. When people buy my labour they must cover my costs of providing for everyone else.

My work and the work those people are doing needs to pay all those costs. We effectively pay eachother to work at what we are independently good at - trade.

But a worker only receives revenue from the work they do (I'm excluding unearned income)

If everyone gets everything they need ultimately from other people, and each of those people needs to get everything they need from everyone else - and sometimes the same people.

Where does the salary of the workers I buy things from come from?

I feel intuitively it doesn't matter how much bread someone can create, the total revenues from selling bread in general needs to cover the costs of all their employees and the business costs themselves.

But this process repeats for all transactions the total transactions for MasterCard pays the bills that MasterCard employees have.

Everyone needs to earn more than they cost but so does everyone else! How can this not inflate endlessly over time?

When I look at government deficit and debt levels of the world, people don't produce more than they cost and relative and absolute poverty.

What's the proportions of owners of wealth? Compare the bottom 99% with the top 1%.

In fact, you could make the argument that all of human endeavor is simply withdrawing from the bank of 4.x billion years of sunlight.

https://astralcodexten.substack.com/p/your-book-review-progr...

Farmers don't have to pay for the energy used to grow wheat. The Sun provides that for free. Same with the oxygen, and much of the water. Value is created, it's not a zero-sum game (except from the perspective of universal entropy.)

In a healthy economy, most of the value should be created rather than extracted from others. But ownership of fixed resources like land led to serfs and sharecroppers, which led to landlords and industrialists accumulating capital, which led to exploitation. That's Marx's whole thing.

The farmer doesn't pay the sun but they still have to pay other costs ad infinitum. There is no last cost.

Each of those people also have the same problem

I'm not arguing for zero sum. I'm just saying that the problem of costs is recursive, you need to produce more than you cost. As each of those people has the same costs that I do. So it can only grow in size and costs can only inflate.

Society requires everyone to produce more than they cost. The government invests in you in terms of free education and in some countries free healthcare.

Work is the resource that is renewable. Everyone is forced into a grind to raise enough to pay for everyone else's costs and your own due to the recursive relationship of costs.

I am arguing that in a society each person needs funding from somewhere, it can only come from everyone else in exchange for their work. Each person therefore depends on their costs being provided by everybody else. This relationship is therefore recursive. As each person must also provide for everyone else that someone is providing for.

As we witness in the world, not everyone can produce more than they cost. Some people cannot afford to travel or stay near work. Opportunities are cut off from them.

These people are desperate and have no capital. Money is a time machine and if you have none of it you are forced into grunt labour.

You don't get 100 million working as a pizza delivery driver or delivering parcels but the owner sure does.

https://nypost.com/2021/06/26/san-francisco-run-homeless-enc...

And we also witness that others can produce more than they cost. So it could (actually, is and has been for the last ~500 years) be that overall, the average person produces more than they cost. Forget your recursion idea.

TL;DR – Yes, but the added value gets smaller each recursion, such that even if you add on an infinite amount of these costs it will only come out to a finite value. The productivity of a single person, which in today's industrial world is immense, makes these costs so small they might as well be cents on the final product.

Let's say a farmer farms a square field with 100 metre sides, or exactly 1 ha of land. This is a size which it is perfectly reasonable for one person to farm, even entirely by hand, and which is woefully small considering modern farming equipment. On it they grow wheat, with a production of 0.25 kg/m² annually, or 2 500 kg when you do the calculation. This is a perfectly reasonable yield. Taking into account milling yield, we end up with only about 70% of that, or 1 750 kg of flour. A loaf takes roughly half a kilo of flour so, assuming water and yeast are effectively free, so selling this to a baker, they produce 3 500 loaves in the end.

So far, so easy. Then we take into account the losses that are going to be accrued for the loaf of a single customer in this very small thought experiment economy, in which exist only the farmer and the baker. Each, we say, might eat 2 entire half-kilogram loaves in a week, so 8 in a month and 96 in a year. The baker prices one loaf at (flour cost + 96·loaf cost)/3 500. The farmer prices his flour at 96·loaf cost/1 750 kg, but as the farmer buys everything, we can ignore the division. The price of one loaf is now (96·loaf cost + 96·loaf cost)/3 500, or 192·loaf cost/3500, or, rounding a bit, 0.05·loaf cost. Propagating it down, we have 0.05²·loaf cost, then 0.05³·loaf cost, and when you recurse to infinity, we have 0. The further you get from the producer, the smaller the added cost becomes in reality, such that even if you add up all the costs you eventually reach not an infinite value but a finite one.

If we say that each take a profit of $100 annually in addition to what they need to live, we get that the farmer prices their flour at ($100 + 96·loaf cost)/1 750 kg and the baker their bread at ($200 + 192·loaf cost)/3 500. Propagating it down, the price becomes ($200 + 192·($0.06 + 0.05·loaf cost))/3500 = ($210 + 0.05·loaf cost)/3 500. Going further, it will be ($210 + 0.05·($0.06 + 1.4·10⁻⁵·loaf cost))/3 500 where we entirely lose precision and the added cost from profits appears to stay at $210/3 500, while the rest of the calculation becomes so small it disappears off to 0 at infinity once again.

While this example is only very simple, and I won't prove here that it applies in larger or more complex cycles, it is nevertheless fairly obvious that this disappearing off applies to everything. Whereas your recursive argument about costs only being able to inflate is correct, they can only inflate up to a finite value at the limit due to the inflation added at each level of recursion being smaller than the last.

What I witness in the world is endless costs, from housing maintenance to shelter and rent and mortgage costs and transport costs. Everything is very expensive. Housing is not cheap relative to salaries nor is transport.

If I wanted to pay someone to do work for me, I need to pay enough to pay all the workmen's costs.

I need to provide for myself and provide enough revenues for everybody else to pay for these things. So the prices you pay provide revenues for these costs fans out in all directions through everyone you buy things from.

Is the finite value that these cycles larger than the money supply?

There is a finite amount of work that can be done per period of time but some people work 60 hour weeks. But work is renewable until you ruin your joints and knees or health problems.

I am sure everyone wants to earn more and has costs they want money for and want larger houses and to own housing rather than rent.

I didn't even include profits or value addition to my theory as they need to come from somewhere.

I think you're correct in that everything is very expensive, possibly close to the most expensive it can be. Salaries paid are essentially just what is enough to keep yourself alive nowadays, often not even enough to keep yourself in decent mental health. I doubt your average worker is capable of purchasing everything they create in a month with their monthly salary.

It's certainly not the first time this has been observed either. Let me give you a classic criticism. Take the old but reliable labour theory of value. We ignore price fluctuations for this analysis because they are considered nothing but representative of true value – a method of making trade easier. Work is what people value, specifically the time used for labour. Creating something in one minute gives it one minute of value, it would be more valuable if it took more effort to create. For the purposes of markets, it's also obvious that what matters to us is not the individual value per se but the socially necessary labour time, the average value taken to create something. Therefore a man who creates a spoon in one minute and a man who creates one in 20 will make an equally valuable object in the societal context. Creating an object from materials will have the value of those materials plus the value you create through your work, so $2 bread from $1 wheat will have $1 of additional work done by the baker.

With this in mind, let's investigate farming. A farmer works land, they create $1 worth of wheat and sell it. That $1 is the full reimbursement for their work and if they want to buy their wheat back they will pay that $1 for it.

Adding in an agricultural conglomerate, lets say that a bunch of farmers work the land of this conglomerate as employees. As a large oversimplification, we once again say that a farmer creates $1 worth of wheat for the company. The company sells it and returns to pay the farmer a salary: ¢80. The ¢20 missing is the profit of the company and it has to be larger than zero for the company to keep existing at all, profit being their singular reason for existence.

This is fine and all, and it's how most companies work, the issue arises when you think about the farmer being a consumer. The farmer is not reimbursed in full for their work, in other words, they become incapable of purchasing back their own labour in full. If the farmer the goes home and to the store, they cannot purchase the wheat they themselves created, it will cost more than what they were paid. This repeats itself in every company, the employees simply cannot be fully reimbursed for their work, not now and not ever. Yet, the workers also form the base of consumers, they are the vast majority of people who must be relied upon to consume these products. The end result is that everything seems expensive relative to salaries and you will, at some point, have to have a violent economic event to correct the markets as consumers simply run out of money.

Now that's not accurate in its entirety and it's a critique from the 19th century, but it goes to show that we have always recognised this being an issue. We just deal with it by accepting that some people will be unjustly hurt in regular recessions in the boom and bust cycle and move on – there's no just way of doing things without entirely removing companies from the picture. That's the way our economy is doomed to work, and we just have to accept it and move on unless we want to literally outlaw companies and organise production on a national level.

But that revenue-optimizing tax rate, which is the subject to much debate, is probably somewhere around 65% to 70%, far higher than the tax rates in the United States. We could surely increase taxes on high income individuals without doing much harm to the economy.

The thing about the Laffer curve idea that I don't understand is the curve doesn't need to be continuous. Say we accept at a tax rate of 100% you get no marginal benefit from working so no-one will work and the tax take will go to zero, at a tax rate of 100%-epsilon you still get (small) additional marginal utility for each additional dollar earned, so it's still in your interests to work. So it's literally only at a tax rate of 100% that the Laffer concept would make the tax take go to zero.

[1] https://medium.com/junior-economist/the-laffer-curve-6bb2833...

"In practice, the Laffer Curve has not provided the dual benefits of lower taxes and higher revenue. In fact, every US tax cut since 1965 has been followed with a sharp decrease in tax revenue, while every increase in taxes has led to an increase in government tax revenue."

Yeah, that's the point of the curve. I don't think you've made a convincing argument against continuity.

And the quote seems to misunderstand the curve (I didn't read the article). The curve itself is reasonable, the main debate is where the current tax regime puts you - to the right or left of the peak. The other mistake is that many people using the curve to argue for lower taxes are not really honest debaters. They want lower taxes and use any argument available. They state that we're on the right even though ask evidence suggests the opposite.

The only thing that maintains the value of any asset (or currency) is the collective belief in that asset or currency. Put another way: there is an inescapable component of trust in every asset.

Crypto in any form doesn't solve the trust problem other than a very narrow slice because as soon as you interact with anything outside of the blockchain, you're adding trust. Even on the blockchain, all the math in the world doesn't avoid the trust problem (eg it's been estimated that over half the Ethereum are owned by less than 10 entities).

Even backing a currency with gold (or any other asset) doesn't solve this problem. Additionally, it's not even correct. In years long gone the US government just maintained a peg between the US dollar and the gold price. Any reserves (which were never 100% anyway) are irrelevant to this. You don't need them. You just need sufficient capital to maintain the peg. Even if you had 100% reserves you still have to trust the government to honor redemptions and not to change the peg. If you have sufficiently deep pockets, you end up not even having to spend much money because no one challenges your peg.

So what actually makes the US dollar work as a currency is that it is backed by the long dick of the US government. This is a combination of economic, military and even cultural might.

So going back to algorithmic stablecoins, it doesn't matter how much you have in reserve. It doesn't even matter if there's new money entering the system (as this article claims) to maintain the peg. If people lose faith in the "stable" coin, it's finished.

Most non currency assets are cash flow generating financial instruments.

If analysts don't believe a company is worth a dime, it can show them wrong by being profitable and paying dividends.

Edit: I think my point is - even if no one else believes in a stock or bond, you can still profit by "being right". The same is not true for currencies.

I don't think this is very useful, since "yeah but without society there are no companies, money is nothing" doesn't take us very far! But hey.

How does a company make money? Why does it distribute that money to shareholders? Why can't someone working at the company just keep all the money? Why can't the bank just confiscate it?

The answer at all levels is the the threat of violence. Property rights (eg to the money) are enforced by the threat of state-sanctioend violence, for example the police showing up at your house and throwing you in jail if you don't comply with laws.

So why would the police show up and do that? Why would the courts enforce those laws? It's not just the threat of violence, essentially. It's the collective belief in that system.

I'm happy enough to put value in USD or imaginary-coin if I can swap my holdings in them for a nice house/car/jet. You don't really need "economic, military and even cultural might" - just for the currency to be accepted somewhere where you can buy real assets and for the supply to be limited so it doesn't inflate to nothingness.

Without that collective belief, owning anything is a huge effort to defend it against whoever else it might appeal to.

The reason people are willing to give away their house/car/jet in exchange for crumpled is the existence of the market protected by that "economic, military and even cultural might".

Trust here is not in that the some big guns are protecting your cash, it is rather about you trusting that the next day/month/decade people will want that cash about the same as today.

That's because it also has use value (and land use value), etc. Crypto coins don't have any.

>Most financial assets are backed to some extent by real assets.

Negligibly so in modern economy.

I can be happy with a nice rock I found on the beach if I really love it and it's important to me. However, what we are taking about here is are assets which have a wider value on an open market.

If people suddenly stopped believing that living in your location makes sense, the value would drop very much. See ghost towns.

The problem is getting stuck holding the asset for a long period of time. USD will lose 80% of it's value over the next 50 years. Tether likely will lose 100% in that time frame.

Right. I believe the point of the post you replied to is that while it may be "valuable to you", it also may or may not "have value" (which I interpret as being exchangeable / interesting to other parties), which requires common belief/faith that it has value (basically a circular definition). I could be misinterpreting one or both :)

It surely is, but this is just a semantic play on the word "value". You mean something like "personally important" in that sentence, the comment you were replying to was using it under its well-established economic definition.

In fact, your house is *not* valuable (in the economic sense) if there isn't a collective belief in it's equivalent in currency. Rather: it is exactly as valuable as the market is willing to pay, which is just a statement of the definition of "market value". That's what "collective belief" means in this context.

Examples have already been posted here. My house has a use value to me because I need somewhere to live. If I lived on a small island off Antarctica it would still have great value to me but perhaps no value to anyone else.

Money is a financial instrument that only has exchange value, unless you count say the use of bank notes for lighting fires or papering walls. It's value as money is entirely by consensus.

Notably not even the government that issues it actually sets it's value. Ask the governments of Venezuela or Zimbabew about that. Yes of course they can do things that affect it's value, like printing too much of it or defaulting on bonds, or consistently paying on their bonds, but the actual value is set by people. When someone sells a product or service they ask for a price, and if someone pays it then that establishes a value for the product relative to other products, and a value for the currency exchanged. What happened in Zimbabwe is people asked for an awful lot of ZB$ for things compared to how many US$ they asked for. Thats what set the value of the ZB$ (and to some extent the US$ of course).

Governments sometimes do try to manipulate currency values through currency controls, but what that actually does is constrain currency flows. If a currency control set a high price for a currency, it will just not be traded as much, only people willing to pay the premium will do so. Those not willing to pay it simply won't and those transactions and that economic activity will be constrained (or the exchange will happen on the black market).

There can be coercive pressure of course, such as Russia requiring companies to hold Rubles, but you could hold a gun to my head and force me to hand over my house at a discount or for nothing. That says more about the use value of loaded guns than about the exchange value of my house. Governments have the ability to take value rather than exchanging it, but even that has it's limits.

The house you and others have mentioned is an easy one. That whole concept of ownership is reliant on an entire system existing and enforcing those "rights". It's the threat of violence that prevents someone from showing up, "claiming" your house and kicking you out.

It's the ability to demand and enforce tax payments in that denomination - with the consequence of not doing that being you will lose property and liberty.

Obtaining the denomination to settle the tax then becomes the discounted option, since the other option is far more expensive.

That alone makes the currency worth holding, since you can always get rid of it to somebody with a tax bill to pay.

As we have seen with Russia that power extends wherever the denomination is used. The US government has 'taxed' Russia anything it holds denominated in US dollars - completely unilaterally and wherever it was held.

But I think a broader statement is that the "long dick of the US government" is the collective expectation for the behavior of major world governments. On the other hand, it's worth noting that US currency is not absolutely stable.

This is false in the general case. An asset means a useful or valuable thing, person, or quality. If something is useful to me, such as food, hydration or shelter, trust is irrelevant. In fact, something can have value to me (perhaps even objective value), even if there are no other agents/persons.

Even where there are other agents/humans, no trust in an asset is required in some cases. Suppose we all can independently verify the use and quality of something (we call this measurement). If that thing has some definite utility to us, the value each will assign may differ, but that thing's value is not dependent on the subjective valuation (Say a morsel contains 15 Joules and I can harvest 9 Joules and you 11 Joules, the value we each could assign differs, yours being greater than mine, but is objectively derived, being based not on trust nor subjectivity. Subjective meaning based on or influenced by personal feelings, tastes, or opinions). Granted, we can not preclude the possibility that someone, somewhere providing a subjective value to this thing, merely that somethings have value, potentially to many of us that is objective and intrinsic in and of the thing itself.

Trust in every asset is, indeed, escapable.

That simplifies too much. There's also the fact that all taxes on income, capital gains, and consumption must be paid in this currency.

It has a very real value, in that if you don't pay using this then people will come and lock you in a cell.

It's not just a collected belief.

I also believe that the government will by force not allow its own currency to be replaced within its borders.

That's a belief in a trusted third party, not a collective belief.

The only thing that maintains the value of any asset is the demand for it.

Where that demand comes from may or may not be belief.

Water has value because there is a clear demand for it, not because anyone believes in it.

As long as there is someone who wants an asset, it has value. Belief is but a cog in the machine.

The issue with most crypto tokens is that its demand only exists within the closed crypto ecosystem in the form of liquidity, not in the real world. This makes is much easier to shake belief.

Having a reliable long term income stream attached, an actual use for the asset and/or a supply which shrinks in relation to the fall in demand is a much more sustainable source of demand.

> So what actually makes the US dollar work as a currency is that it is backed by the long dick of the US government. This is a combination of economic, military and even cultural might.

What many people call fiat is in fact partly a proof of violence consensus algorithm. Practically applied it means the sovereign will create a demand for its currency by imposing taxes denominated in that currency on its subjects and then threatening or using violence against parties that don't pay those taxes. However, that alone is insufficient to maintain the value of a currency. Mr. Mugabe of Zimbabwe surely had no philosophical aversion to using violence to maintain the value of the Zimbabwean dollar, but the collapse in his country's productive capacity rendered that moot.

Thus we can see that another major part of what makes the US dollar work is that the US economy that the US government has the power to tax is extremely large, productive, and well-diversified.

I agree: ultimately government is a collective decision on who gets to do the violence.

As for Zimbabwe, the primary difference it and the US is reach. More generally speaking, we've seen currencies collapse when people have lost faith in their value and what happens is people instead use a different currency (eg the US dollar) because they have more confidence in its value.

You throw this kind of claim without providing proof. Unfortunately, it's a claim I have seen made before (e.g. https://www.financemagnates.com/cryptocurrency/news/top-10-e...) and it doesn't hold any level of scrutiny. Although you embellish it and exaggerate it even further.

This kind of number typically assumes that a smart contract owns the ETH that it contains. Which is not true by the very nature of the smart contract, what it can do with the ETH is programmed in its code and the users depositing the ETH on it are the ones that decide what to do with it.

Then it looks at the accounts that have the most ETH (https://etherscan.io/accounts), aggregates together all centralize exchange accounts, assumes they also own the ETH. Do some quick math and publish a misinformation article ready to be shared by anyone whose confirmation biases are triggered. Bonus points if you can then exaggerate the numbers further without providing any figures and keep the misinformation going.

Some numbers...

There is currently 39 M ETH locked in DeFI smart contracts (32% of circulating supply). https://defillama.com/chain/Ethereum?currency=ETH

There is 13 M ETH locked in the staking contract (11% of circulating supply).

There is 2.5 M ETH locked in L2s (2% of circulating supply). https://l2beat.com/

So that's 45% of circulating supply not owned by any single entity.

It actually does. If the backing is real, the user knows he will always be able to exchange his coin for $1. If the price on an exchange goes under $1, the issuer of the coin can buy it back, making a profit. If the price goes above $1, the issuer can sell. It's a trivial algorithm. Of course, it only works if the backing is real.

Unfortunately having billions in cash is a huge temptation to invest them and make even more profit. That's what Tether did. And now, if their commercial paper is under water, they are insolvent.

The benefit of these: it mimics in person interactions and describes a simple process.

But The trade off is that they only work if they grow slowly and organically, which seems to be contrary to what the crypto space is trying to do.

Hello jmyeet! Unfortunately, I believe this statement, as you have given it, is untrue.

I hear it often, as it is continually and frequently asserted by crypto enthusiasts (and I am not suggesting you are one of those).

-----

For assets, value is grounded in utility (whether to do some useful function, generate some feeling, etc).

Asset price, on the other hand, could be almost anything depending on supply/demand and may be affected by beliefs at times.

It's important to disambiguate price and value. I can buy a superb pair of shoes from a desperate seller for $1, but that doesn't make their 'value' $1 to me or other people. Value can be personal, it can also be societal i.e. averaged over many people.

Indeed if price and value were the same thing, there would be no buyers or sellers, because you would have little reason to go to the effort of swapping two things of identical value to you.

-----

For currency, specifically, national currency where you are living in that nation - the value (and relative price) of a unit of a currency is grounded in taxation enforced by, well... force, by the state.

Taxation generates continual demand for units of currency regardless of individual or collective beliefs.

And in trust in the currency, again, is enforced by... force, by the state. Which prevents unlimited supply (by random people), again, regardless of individual or collective beliefs.

Thus, both supply and demand for the units of currency are set by the state, and supply/demand is what it takes to generate a stable price and mandatory use.

I note you mention trust, and 'backed by...' and 'might'.

However, discussing currency in terms of only trust and not in terms of taxation, misses half the argument. Both halves are essential for the argument to make sense.

Absent a mandatory minimum demand, control of supply of currency (and trust in that control) is meaningless.

In computing terms, you can see taxation + limited supply as a technique to 'bootstrap' an initial price for a currency without needing any shared or individual beliefs at all. It also underwrites the price in the long term, again, without any need for beliefs.

None of this is to say that a currency can't have its price/value shifted around by collective beliefs once bootstrapping / underwriting is in place. Of course it can. But what maintains, inescapably, a certain minimum price (your own words: maintain, inescapable), is enforced taxation.

-----

Going back to the price of assets. Well, you can believe all you want about, say, oil, and your whole country may have a collective belief, or even the planet, but since there is X units of oil needed and Y units of oil in supply, the price will be set by ongoing auction as always, or you can freeze/be stuck in your garage/factory shutdown. Supply and demand. Beliefs can affect supply and demand, of course. But supply and demand are primary, beliefs are secondary and they sit alongside necessity and physical reality.

-----

(Finally - again without wishing to imply you are a crypto enthusiast - a lot of crypto enthusiasts seem to imagine that mathematics has a similar 'force' to states, 'there can only be X coins', ignoring that a) chain algorithms/limits can be changed by widespread consensus b) no one is forcing anyone to use the crypto at all i.e. no physically enforced taxation c) it's trivial to substitute a chain with a duplicate chain (again consensus), as e.g. dogecoin proved rather effectively. They also invariably neglect the issue of needing 'mandatory demand' via taxation. I would speculate this is because the essential need for tax in currency systems, completely undermines the ponzi's disguise as a currency.)

(I use the word 'ponzi' casually here; technically ponzis are zero-sum, whereas crypto is worse - negative-sum, especially for the environment).

You don't need to trust gold or bitcoin. They are verifiable. Don't trust, verify.

Also, the US dollar doesn't work very well, so you're redefining reality. They're constantly abusing that trust and creating way more money than would be necessary or moral.

In scenario where financial system collapses only real currency is skill - if you can make food from something available locally or be helpful like being a medic.

Why would I trade a chicken that I can eat for piece of gold when I can trade chicken for sewing my wounds after being bitten by a stray dog.

Even in failed states gold maintains value. For example in Somalia’s recent past, not only was gold still fully exchangeable but the existing Somali currency continued to work with counterfeit currency filling the vacuum.

What stops gold exchange is not non-existent government but any particularly strong and draconian government that decides that alternative forms of money are a risk to the regime (e.g. North Korea).

Scalable, self-similar, clustering, and long memory are some of the characteristics of the fractal-style randomness of financial markets. Thus, build in safety factors, multiple redundancies, hedges, etc. with those characteristics in mind.

Definitely not a “proof” in the logical sense.

Likely the Vitalik post linked in this article will have some insight.

> While there are plenty of automated stablecoin designs that are fundamentally flawed and doomed to collapse eventually, and plenty more that can survive theoretically but are highly risky, there are also many stablecoins that are highly robust in theory, and have survived extreme tests of crypto market conditions in practice. Hence, what we need is not stablecoin boosterism or stablecoin doomerism, but rather a return to principles-based thinking.

1. "Stablecoin insurers" (in the author's terminology) are not short puts on the stablecoin, because noone has a specific right to force them to buy the stablecoin. Their position (as I understand it) is much more akin to some sort of swap where they pay/receive the difference between the stablecoin and the volcoin

2. Since it's a swap, then their position has 1 delta, so they don't "delta hedge". They need to make good losses on the stablecoin (and collect profits in good times)

3. There is no expiry so they are not long theta. They are collecting carry on the swap

My understanding of the term 'stablecoin' means that it is a crypto 'proxy' to some fiat currency, typically US dollar, just to avoid the actual conversion between crypto and fiat (because of taxes etc). So why isn't there just a DumbCoin(tm) that simply is 1-to-1 backed by the dollars? You give me a dollar, I mint you a coin. Somebody sends the coin back, I return them the dollar.

As far as algorithmic stable coins are concerned, I have no idea what the point is. Largely experimental as far as i can tell (but pretty much guaranteed to fail given how they work)

1. In fact so big now that cash managers and corporate treasurers keep an eye on Tether as they have a material impact on the bills and CP markets.

Eventually you will get tired of the work and costs involved in maintaining your dumbass coin in perpetuity for no benefit.

Those exist (like USDC), but they rely on a trusted entity holding the reserves.

Q: Where would you actually keep the dollars?

> 1. There must be a transaction tax for real utility provided by the Stablecoin.

Don't all major reserve-based algorithmic stablecoins charge some kind of minting/redemption fee, to reward the risk taken on by reserve holders? And that makes this whole argument somewhat moot, since it's not a purely closed construct like they're describing. Though perhaps this line of reasoning (equivocating to other financial constructs) could lead to fee pricing equations required for some notion of stability.

Then theoretically as long as there is demand for this coin, it will go up in price and therefore can back any sidechain coin that will grow slower in price (or better yet, gradually drop in price relatively to it like the dollar).

That’s what we are planning to do with Intercoin:

https://community.intercoin.org/t/intercoin-application-virt...

No, that is not the definition of a Ponzi scheme. A Ponzi needs funding from outside money to continue to operate, but not everything that needs outside funding to operate is a Ponzi scheme.

As an example let's create a gambling system. Any deposits made into the house account gives you a proportional share of the profits of the system. If the house gets lucky investors can make money. If they are unlucky the house account can run out of money and require outside money to work again. This gambling system isn't a Ponzi scheme at no point are you paid out with new investor's money. If you are lucky you are paid out with gambler's money and if you unlucky your investment goes to 0.

Edit: Even with a positive house edge the house can get unlucky and go bankrupt.

More relevant to stablecoins:

If the stablecoins need constant funding then what is their real value? Why should someone hold them? Why spend them? Why owe them? Constant funding itself isn't bad as such but how much and how often are what decide value.

This is not to say they are useful or useless. But it certainly seems like the market hasn't got a firm answer either. The greater market is at least certainly ambivalent about them.

Contrast what would happen if any of these stablecoins were used for purchasing crude oil or wheat or some other international commodity. In that case we'd see very different views on their value.

> Investments that are provably problematic should be appropriately regulated and efforts should be made to protect consumers against them.

Not at all. Regulate yourself and don't buy things that exceed your risk threshold, or if you are a child incapable of that, tell your parents to regulate you.

If stablecoins are a pyramid scheme, the USD is too. Virtually every currency is negative-sum, destroying value every time they are spent.

…

> Virtually every currency is negative-sum, destroying value every time they are spent.

What?! This is not even remotely close to accurate.

It's being conflated with the word "pegged".

Pegging something to something else that is unstable doesn't make it stable.

For as long as monetary policy in fiat continues to ease, you'll have more dollars around, inflating the money supply.

The pegged item will need to match this in the long run to maintain the peg. Which won't be possible without further minting of the so-called stablecoin.

The real solution, which I admit is a long time away, is to just stop using fiat and their "stablecoin" proxies altogether and just use another currency altogether.

The sky is the limit with Algorithmic stablecoins and you can't throw the baby out with the bath water. All this is simply not true in every case.

Imagine a stablecoin over-collateralized with interest bearing crypto (basket of POS coins) and certified tokenized REITS, synthetic S&P, commodity futures, etc.

An algorithmic stablecoin with a backing system can survive some stress. What they can't survive is a net outflow, because they can't reprice downwards. The era of "line goes up" is now over, and we see net outflows in many financial sectors.

A lot of faith-based financial instruments are going to tank.

Just like driving a car proves impossible without continuous manipulation by its driver.

Is that really a position you want a non-democratically elected agency to have? Society at the behest of Jerome Powell?

Seriously though this is a very wrong analogy. The economy is more like an ecosystem where individuals interact with themselves & the environment. It doesn't need continuous manipulation. In fact it tends to distort than aid.

Which leads to the inevitable conclusion - the US dollar is a simple public monopoly, and therefore monopoly rules apply.

[0]: https://www.c-span.org/video/?c4454549/user-clip-bernanke-ag...

The idea behind prices in a market economy is that they're an information-carrying abstraction. They let producers at every stage of the value chain understand the relative costs that go into different alternate ways of producing a good, without needing to understand every single stage of the supply chain and all the decisions that their suppliers made. And it also gives them information about relative demand, so that producers which make things that nobody want go bankrupt and those make things that lots of people want rake in windfall prices.

The whole point of the Fed is to alter prices, on one hand to keep producers from raking in windfall prices (price stability) and on the other to prevent too many of them from going bankrupt all at once (full unemployment).

Problem is that when you do this too much, for too long, the biggest input to a firm's production decisions becomes the Fed funds rate. When it goes up, time to layoff people, because the cost of capital just went up and you can't do anything without capital. When it goes down, time to go on a hiring frenzy because if there's money for the taking and you're not the one taking it, you get outcompeted by the ones who are. Over time this begins to dominate all other signals that pricing normally provides, like producing goods efficiently and making things lots of people want. You get companies like Uber, which lose money on every transaction but make it up in fundraising.

In turn this increases sensitivity to the Fed's actions, which limits their freedom to take them. If the whole economy breaks when you raise rates to 1.5% (as happened in 2019), it becomes very hard to raise rates above 1.5%. So rates get pegged below the natural rate of interest (which equilibrates supply of savings with demand for productive investment), lots of economically dubious projects get funded, you inflate a perma-bubble, and you can't deflate it without taking down the whole economy.

Beauty is in the eye of the guider.

I don't believe that's the case.

However, once you've put your hand in the meat grinder of debt, what you just said becomes a self-fulfilling prophecy.

The stablecoin on the other hand claims that stakers are being rewarded for risking their capital without holders of the stable coin being fleeced at their expense. The only way to do this is by the number of people coming into the system expanding, and unlike the gambling system, the proposition of the stablecoin is these new participants don't lose money either. It has the classic Ponzi dynamic of being a zero sum game masquerading as a positive sum game through growth.

I guess a stablecoin could theoretically operate on the basis that "stakers" were supposed to enjoy average negative returns for the sheer joy of gambling like people on craps tables. That would be much more like your proposal, and would be far too truthful in its white paper to be called a Ponzi, though it might have trouble attracting gamblers compared with the glitz and glamour of the casino and all the crypto ways to gamble money that don't openly admit paying negative returns.

They mitigate the risk by settings caps to maximum bets. You can't just bet a bit more than half of a casino's assets in double or nothing with them. They don't want to be taking a 50% chance of losing everything. Even if there was a 2% edge that's still a 48% chance of it happening. They would rather work with smaller amounts where the chance of someone winning a ton of times in a row to eventually win everything is practically 0%.

>The stablecoin on the other hand claims that stakers are being rewarded for risking their capital without holders of the stable coin being fleeced at their expense.

They may be rewarded but they aren't being guaranteed that the value of what they hold will always go up.

Again a Ponzi scheme is a very specific thing. People make an investement and returns on that investment come from new investors. In this kind of stablecoin system there is no part that where that specific thing happens.

>were supposed to enjoy average negative returns for the sheer joy of gambling like people on craps tables

This is usually how algostables work. People bet on growth of the project and once growth has peaked negative returns will be coming. By trying to avoid this period of negative returns a depeg happens.

Enforcement is an interesting factor. Laws can guarantee rights to enable and protect free exchange, but they can also coerce behaviour as I touched on.

In more or less free markets what laws do is provide guarantees that increase trust, which has the main effect of reducing costs. You don't need to personally audit the books of a company you invest in, because the government mandates that it's done for you to a set of standards which eliminates some risks (not all, just some). You don't need to personally research if the products you buy are safe or of a basic level of quality if the government mandates standards and enforces them, and if you have a right to return goods if you find a problem with them. This makes the goods themselves a little more expensive, but the overall costs and risks (which translates into costs) to consumers are much lower.

A different belief shifting, though, would change the equation dramatically: either a shift towards less exclusive property ownership (e.g. theoretically requiring any non-primary residence to be rentable or something crazy like that) or dramatically higher tax burden for non-primary residences. If the annual upkeep costs were to increase, the external value wouldn’t change much (it’s already pretty close to zero), but the intrinsic value for us would drop dramatically and we might consider dumping it.

Trust keeps bank runs away, arbitrage keeps the peg tight (feeding into said trust).

This means that you cannot look simply at total ETH issued from the genesis block as you will be overestimating the amount of ETH in circulation by the total amount of ETH destroyed through base fee burning. Currently around 2.4M ETH has been destroyed in this manner.

The figure I gave above (~120M) includes all other ETH. I.e. All ETH that exists. Including ETH that perhaps has been forever lost due lost keys or sent to wrong addresses or addresses that nobody has the keys for (e.g. https://etherscan.io/address/0x00000000000000000000000000000... or https://etherscan.io/address/0x00000000000000000000000000000...)

So for all intents and purposes circulating supply is total supply.

> Again a Ponzi scheme is a very specific thing. People make an investement and returns on that investment come from new investors. In this kind of stablecoin system there is no part that where that specific thing happens

The returns on staking do come from new investors. As you point out in your next comment, they turn negative after the project stops growing.

I agree it's not a Ponzi scheme in the narrow sense that some mountebank is telling stakers that they're being paid from the profit of nonexistent businesses before running off with the money. But the dynamics are identical: as you point out in the next post, the project depends on stakers earning rewards from its growth and the scheme collapses when the project stops growing and the stakers seek to avoid losses.

The dynamics of a casino are different: it doesn't promise its gamblers a positive return and thus doesn't needs constant capital injections to survive. Gamblers are service consumers, not investors and betting for entertainment that the wheel will stop on black, not for profit on the casino's ability not to default.

2. You vastly overstate the power of the chairman of the Fed. It's not like Powell can have a bad day and decide to nuke the world. He's more powerful than most people, but society hardly depends on him.

Just imagine someone like the 45th being able to order the Fed around in a way similar to Erdogan. Complete, utter horror.

> However, since Trustlines is designed to be implemented on a public blockchain, making transactions requires the use of a native cryptocurrency to pay transaction fees.

But this one part seems wrong. With such a design there should be no need for global consensus. :(

But the whole point of a corporation is it is a legal entity, you don't need to trust anything for it to work other than other than.. idk the fabric of our society.

I think I read something similar in Sapiens.

This is my takeaway from the book The Case Against Reality.

This reminds me there always exists a path between the current society & a completely different one, and a short path to something completely different is to start from scratch.

A company exists and has valid standing not because people believe in it but because the law says it exists. It is easy to prove beyond reasonable doubt that a company exists (or not). That has nothing to do with whether people believe it is valuable.

In the case of DAI and other debt-based stablecoins, there is no minting of additional collateral when liquidations occur or when debt is repaid (the total amount of the underlying collateral in circulation does not increase when DAI is destroyed).

This is the main difference between so-called "algorithmic stablecoins" (e.g. UST, FRAX, USDN), which rely on internal collateral (whose supply can be arbitrarily expanded/contracted by the controlling entity) and "overcollateralized debt-based stablecoins", which usually rely on external collateral (whose supply cannot be arbitrarily expanded/contracted).

Treating these two different things as if they are the same is not particularly insightful.

No, the idea behind prices is that they are what the participants in particular trades think it is worth trading at.

The normative argument for the superiority of laissez-faire economies may involve market prices as an information carrying mechanism, but that normative argument is much newer than market economies, and is not the “idea behind prices in a market economy”. The benefits some people see (or imagine) in something after the fact are not the underlying purpose of the thing.

> No, the idea behind prices is that they are what the participants in particular trades think it is worth trading at.

Why are these two things mutually exclusive? Aren't they, in fact, mutually dependent?

They aren’t. They are different, and one is actually the “idea behind prices in a market economy”, and the other is an academic argument, observing the fact of price setting in a market economy, for why price setting in a market economy is valuable to others besides the direct participants in the individual exchanges.

> Aren’t they, in fact, mutually dependent?

No, there is a one-way dependency between them. The normative argument depends on the fact, but not vice-versa.

But the only body even attempting to determine what "productive investment" is and respond to it is the Fed. Savers are interested in money returns or at least preserving their holding which in many feasible circumstances (chronic instability, zero sum economies with fixed currency supply) is most reliably achieved by not investing in anything productive, not whether their investment makes optimal use of a country's productive capacity. There's nothing more "natural" about production decisions taking the spot price of a commodity the monetary authority has designated as money, or an arbitrary growth rate for money, or how badly undercapitalised wildcat banks are as inputs, and there's nothing about a regime not trying to avoid bubbles or busts that makes it inherently less likely to result in them.

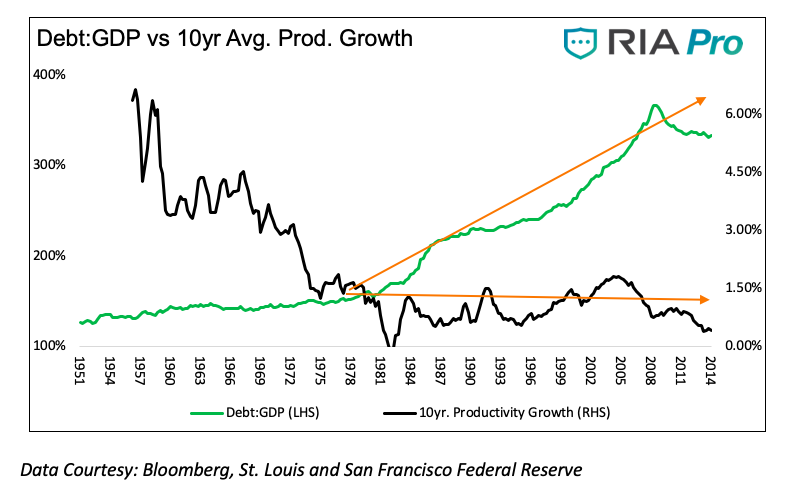

Peter Thiel and many other observers have noted that American innovativeness and productivity growth fell off a cliff c. 1971 [1]. He blames government regulation; however, a more likely explanation is that Nixon turned the U.S. dollar into a fully-fiat currency right around then, incentivizing people to compete for newly-created dollars rather than capture more of the ones circulating through the economy.

The causality might run the other way around too, as the Fed holds rates artificially low to paper over low real productivity growth, but this is not an improvement: it just means that we have a feedback loop between money-supply growth, inflation, and low real economic growth.

[1] https://www.seeitmarket.com/wp-content/uploads/2019/01/debt-...

Or you decide the winning move is not to play, because borrowing is expensive, the purchasing power of your Benjamins won't diminish if you bury them in the ground, and investing money on capital goods in the hope of accumulating more money has negative average risk adjusted returns if there never is any more money in aggregate. On the other hand the way you capture the share of the growing pie is by increasing efficiency, it ceases to be an adequate investment strategy to just hold your capital in uninvested currency.

And taking a graph like that one where the sharp fall in productivity growth starts a couple of decades before leaving the gold standard and actually stops falling afterwards as evidence that leaving the gold standard caused productivity growth slowdown is peak gold bug dodgy graph interpretation! Bretton Woods collapsed because it was inherently unstable anyway.

Now Charlie gets $10 dollars as credit (not the same as cash) from Alice (mediated through Bob) and wants to buy $10 items from David and Eve. He shows the letter saying that Alice is good for the cash. Without a distributed consensus method, how can David or Eve confirm that they will be able to go to Alice to collect the cash? How can they even know that Alice has the cash in the first place? What if something happens to Bob?

The only way to do this without a blockchain would require something like Paxos, but Paxos only works if the participants are selected a priori. Every new participant would have to be vetted by everyone else, or everyone else would have to follow some central authority that can grant access to the system. If you are going this route, you are just re-inventing a credit cooperative.

If something happens to Bob, too bad. Both Alice's and Bob's IOUs are void because Bob can neither pay up nor demand payment. Both Alice and Charlie are sad because they knew Bob, and their ability to trade was more valuable than the current balance.

You can remove Bob from the scenario and the problem still stands. Say that Charlie gets the IOU directly from Alice, David and Eve are left with duplicate IOUs. Alice has trusted Charlie with $10, not $20, so she can not re-pay both of the creditors. If you say "David and Eve should not have trusted Charlie then, so too bad if they lost each $10", consider the systemic issue if the double spending is made against with thousands of participants.

Without a way to control for double-spending, everyone can mint IOUs freely and any credit note is essentially worthless. And if remove the idea of IOU and try to make all transactions "cash-based", you just turned a fungible-currency into a non-fungible one (are these $10 coming from Alice-the-good-creditor or are they coming from Dick-the-double-spender?)

This, taken literally, is clearly false (the wealthy do in fact buy things and pay for services / employees).

So, as you don't mean it literally, what do you mean?

You save on buying in bulk and using better made products with longer lifespans, afford better education that makes you more difficult to fool and gets you a higher paying job, make more returns by investing more money, conserve willpower for important decisions by not having to choose between soap and bread at the store.

>> The economy is not like an ecosystem since there is no reciprocation If mutual beneficial trade is not reciprocation, then I don't know what is. Reciprocity is more a societal thing than an economic one. I would say historically there have always been reciprocal societies. Smaller ones tend to be more reciprocal than larger ones since their survival depends on it.

>> Money flows in one direction only, toward the top This is by design i.e intervention. It need not be so. And there is nothing preventing a species from colonizing an habitat till it exhausts the resources and it's own ultimate demise.

Monopolies, by and large are formed (and broken) by government aid/intervention. Post the industrial revolution, the government has become involved in more and more areas of the economy, so much so that now it has become the chief driver, to stimulate growth, reduce inflation, boost employment/industries. Given the complexity of interactions in the real world, I don't understand how someone can believe they can understand everything and control it.

Regarding your other comment, I agree, the notion of exponential growth is ridiculous and runs into real world limits.

So natural monopolies and economies of scale are caused by governments?

> cue autonomous vehicles

In my analogy, the driver can be a machine.

> Seriously though this is a very wrong analogy. The economy is more like an ecosystem where individuals interact with themselves & the environment. It doesn't need continuous manipulation. In fact it tends to distort than aid.

It does if you want to to go where you want to go. Take that away, and it'll drive off a cliff. Maybe eventually it will correct itself, but that'll take too long to help us.

It's perfectly true that the system is perfectly capable of running alone without any external stimulus applies. The economy will keep being the economy no matter how much you tamper with it. The main problem people have with that is not that the economy won't "work", it's that the economy working necessarily means things like heavy business cycles, cyclical unemployment, a general tendency of wealth to move upwards, and a relatively fast accumulation to the level where those who have accumulated wealth begin to have serious power over politics and will impose meddling with the economy for their benefit.

It will work fine, it working just isn't what humans generally want to happen.

The idea that your wealth ought to grow exponentially regardless of whether the economy itself is growing and how much you contributed to the economy is ridiculous. What did people expect from this arrangement other than accumulation of wealth at the top?

By the way, the economy won't work, it will collapse at some point, because 3% growth over two thousand years would imply colonizing entire galaxies. People think they have a birthright to eternal 3% growth without even being aware of what it means to grow exponentially for that long.

It's possible - just it represents a significant amount of work that needs to be invested in the product before it can see the light of day (compared to other domains where there's less needed to invest).

However, I posit that all of those downsides are inherently necessary to drive innovation and increase the efficiency of the economy. Bankruptcy and unemployment is how you garbage-collect inefficient ways of doing things: you want people to lose their jobs, because that forces them to take employment in more efficient sectors of the economy. Hoarding is how you a.) amass the capital stocks so that you can deploy them on bold opportunities when they arrive and b.) ensure that people are selective about which opportunities they pursue. If you encourage people to immediately invest any spare cash because the value of that cash goes down, you encourage them to seek out any marginal-productivity activity that might remotely be cash-flow, rather than waiting for big innovative opportunities that might take longer to appear.

In other words, I'm saying that there's no free lunch, a concept that should be familiar to any economist. You need failure to drive success. Mitigate failure and you also eliminate success. And the opportunity cost of suppressing serious failure for 50 years is stagnation, low productivity, and inflation, exactly what we've observed. All social systems eventually collapse; it's just that some people who remember how the previous social system collapsed become blind to how the current system is collapsing, because all they can do is think back to the problems it solved.

But the United States is not the world, and the latter half of the twentieth century is not all of recorded history. The majority of the world grew further and faster over the period of modern money than at any other time in history (yes, there are other important reasons. There are other reasons why US productivity growth is not at its postwar peak too). The majority of recorded history on commodity standards, owners of wealth didn't patiently wait for the most innovative opportunities and direct resources better than the modern world, they hoarded, barely maintained their limited capital stock and much of the speculation that did take place was on capturing neighbours' hard assets rather than generating new wealth streams. US productivity growth in recent years might be below its postwar peak but is way ahead of historic norms, including the initial period of growth and labour saving device invention so unprecedented we call it the Industrial Revolution. Which doesn't mean the current system is ideal, it just means that everybody was worse off before.

https://economicsfromthetopdown.com/2020/01/17/debunking-the...

Their argument is what the graph is actually showing is related to the fact that labour's share of US income peaked around 1970 and then began to drop, not some tautologically-defined concept of "production".

Without any transitive property, "Charlie gives his own IOUs" already exists. It is called "selling on credit". No crypto required. Shop owners have been doing that for centuries with pen and paper.

Alice wants to buy an apple from Charlie. Alice gives an IOU to Bob, Bob gives an IOU to Charlie, Charlie gives the apple to Alice.

And - sure, everything crypto does could be done with pen and paper and a phone line. But here Bob's computer can agree to do this without Bob's involvement.

It's feels very similar to a game. A serious one at that, with real consequences. It does not have a clear winning and/or losing condition though.

Whereas for your house, no matter what its market value would be you still have the right to live there and prevent others from doing so.

Anyone who's lived through a massive societal upheaval, collectivisation, dictatorship etc can attest to this - your ownership of property only means anything in as much as it's protected. If the state fails, or if society's understanding of private property radically changes then your investment is only valuable if you can hold on to it.

Even in the private-property loving West the value of an individuals property can often turn out to just be the amount that the state decides to pay them when they seize it via eminent domain.

If the value of _dollars_ goes to zero, the house doesn't collapse. The social consensus and enforcement mechanism that protects your right to live there probably does though

That is, the reason that you can call the cops when strangers take over your kitchen is because we have a very real police force, whose are permitted (even required) to use force in order to protect your property. Property may have started out as a collective belief, but the processes put in place over the last few centuries - especially the concept of Rule of Law [3] - have made it very real.

But ISTM that crypto works outside of these norms. From what I can see, it has no effective rule of law; no possibility for the creation of an effective enforcement body. There appear to be no consistently applied consequences of cheating, either intentional (eg, rug-pulls) or not. People seem to steal money using crypto scams all the time [1]; from what I've seen of it, the world of crypto seems to pretty much embody my personal, nightmare interpretation of anarcho-capitalism [2].

So while I agree that property is a collective belief in theory, in practice it has the rule of law, the legitimacy of the state, and the monopolisation of force supporting it. Crypto seems to have none of these things supporting it; I'm yet to be convinced that it is even, actually, property.

[0] https://en.wikipedia.org/wiki/Legitimacy_(political)

[1] https://web3isgoinggreat.com

It has been translated into laws and social contracts backed by established enforcement that is sufficiently effective and has been demonstrated to the satisfaction and judgment of most people.

It's true that in the event of nuclear war, this could all evaporate --- but this probabilty is low enough for most people to reasonably ignore. Labeling this a "belief" is thus somewhat disingenous in the fact that it is reason rooted in logic and judgment and probability.

If you find yourself believing that our own social contract is the only logical & rational one, or at least the likely result of social progress, you might try reading Graeber and Wengrow's The Dawn of Everything. It covers a very wide range of alternatives that all made sense to the people in those societies at the time.

The "logic and reason" here has to do with the fact that the social contract is sufficiently real and functional enough to transcend mere "belief" in most people's lives.

So, the "long dick" of the US government that grand-parent was talking about. Society creates value.

In a sense, it sounds like a political party that splits in two. It’s not democratic; maybe it’s technocratic.

In early crypto days there was a general feeling that the "power of math" (i.e. how hard it would be to break various hash/public key algorithms) is the enforcement body and the reason you don't need a government and a police force. Maybe smart people saw through that, or maybe the experiment just had to be done to see how this actually turns out in practice.

Your points are why I thought an official US crypto coin could work. But there is not that much net added value compared to what credit cards offer.

Personally I think the question of political legitimacy doesn’t make the notion of blockchain governance wrong; it just highlights that the system as constructed may have problems.

Societal contracts are just collective beliefs. When the number of people upholding a particular societal contract goes to zero it ceases to exist. Just as any other belief, it requires believers to exist. Unlike, for example, the space rock that some group of sentient organisms decided to call Mars.

Another thing, if you want to make transactions like the one you described, you don't need to pass IOUs around, you just pass money. Alice gives the IOU to Bob, Bob gives her money and then she can buy from Charlie, David, Eve or anyone else.

What is the scenario you're imagining of Alice attacking Charlie?

What you want to do is an digital version of Hawala. Hawala works, but there is a reason it is not automated. You can not scale it and it gets very easy to hit liquidity bottlenecks.

I think your ideas are in the right place (if you look at Raiden's off-chain side payment channels, it works somewhat similarly with what you are attempting to design) but can we agree to the fact that if they were feasible to be done without BFT mechanisms, it would have been done already? It is not like people want to use blockchains.

What are these liquidity bottlenecks? Feel free to reply with a link or a keyword if this is common knowledge.

One thing I like about this model is that you can have regular fiat money on top if Charlie gets his IOU from the US government and Alice gives one of US government IOUs back. But it can now be a single network for all currencies where anyone can start issuing their own money.

> can we agree to the fact that if they were feasible to be done without BFT mechanisms, it would have been done already? It is not like people want to use blockchains.

I'm not sure. Would anyone be able to profit from it? Developing the software and educating people is hard, especially with p2p things.

Re: profiting from the Blockchain, you are going at this backwards. You don't need to make it profitable by the tech. What we want is to have a global payment network that can make transactions cheaper than (and equally faster/secure as) Visa. If that were possible to do without blockchains, the market would pay handsomely.

{kind=link}