Europe's $24T Breakup with Visa and Mastercard Has Begun(europeanbusinessmagazine.com) |

Europe's $24T Breakup with Visa and Mastercard Has Begun(europeanbusinessmagazine.com) |

23% of people in Poland, assembled luggage in case of war. Yet EU is still buying russian gas and oil.

and they don't have permissions to military to pass through in case of help from country to country

I hate having to use visa or mastercard when better options exist but the solution is to allow competitive solutions and make surcharge mandatory so customers bear the cost of their payment choices.

In the begining of this year, they basicly banned EU merchants from using confirmo (crypto payment gateway), when it was finally getting traction.

Will it be accepted in hotels abroad? Can i withdraw cash at ATM abroad? Can i add it as a card to my Google wallet?

Usually banks app are nightmare. Pins everywhere, extra passwords. MFA not with my dongle....

Sigh.

Seriously, I have had no issues with visa or mastercard. This euro-nationalism is odd to me.

Oh! That's exactly what we all needed - 16 banks suggest their own "system", even more crude and clumsy imitation of the surveillance standards of payment systems and marketplaces, which shielded banks from snitching clients' consumption patterns.

They don't need anything advanced like Apple Pay layered tokenizations that at least respects a little of privacy. Everything is linked to a single phone (the article states that the focus is on Bizum and those pathetic peer-to-peer payment systems). The banks are in good shape to capture data, the tax authorities have a clear picture of how to squeeze the plebs even more - nice.

How about stablecoins with native yield from ECB treasuries? It solves everything and costs nothing. But we see what happens in US - "treasuries spread is not for plebs", - banks say.

I am also about to score life time golf status at one of the airlines. Yes thank you

Now, what will happen in the UK.

I have a recent background as a member of the Senior Management of one of the largest banks in Europe (8 years stint).

I worked in IT - and build the only successful platform for financial services done in-house and to ever make it as a standard not because management tried to force people, no because it solved customer's problem (external and internal customers aka employees).

I don't buy any of these EU is going fully independently. EU's IT isn't capable of doing this. No way ever ever.

I will 100% of the time bet against it. I saw so many things, experienced so many things - and no way is there anyone out there in Europe who to this day simply can acknowledge and appreciate the marvelous work and evolution that for example Google took or any other startup to leading global business like Apple, Facebook, Microsoft, Amazon and so on.

Even IBM's mainframe: if you do not understand the very problem they solve - don't talk about "independence from X".

There is no successful startup from Europe, that has any results like the mentioned. All have to do with IT, all went from idea to what they are now.

And Europe now wants to do what?

All my fellow European's here boasting around: I feel sorry for you. All the "Let's build our own Google" (Google search) folks that predated the other independence stories like this here simply disqualify themselves the moment the say out loud such sentences.

Read 5 books about Engineering at Google, read the HTML5 spec by searching for Ian Hickson, go to the Computer History Museum in Mountain View, CA - and tell me that EU is going well in IT independence in taking a totally different approach, ignoring every and any circumstance and context the mentioned companies had, using design by committee, state dictated orders, establishing standards by enforcing them by law instead of evolution and being the best there is.

Good luck, we will see how it went.

And no, building something that looks somewhat okish from the outside, but is utterly crap inside - we talk about, excuse me my corporate language I was penetrated with, "best in class world leading number one" apps that leave any comparable solutions in the dust - just as Google, Apple, Microsoft etc. did.

If you cannot win in free markets - you declare victory by misusing regulation. That's cheap and well, socialism.

All of you will beg that all the systems and providers will still do business with you after years of trashing them.

Are Mastercard etc. awesome? Are they objectionable? Of course - but trashing them, boasting you will easily beat them while having the double standard on relying on them freely is disgusting.

All EU patriots: Throw away your iPhones, deinstall all the US apps - use at least existing Open Source alternatives. Cancel your Netflix, Microsoft Office subscription - do it.

Good luck anyway. After all, you are doing a live experiment on the head of the people forced to live with a minorities decision.

/s

Visa/Mastercard are the biggest evil. Why do you think Trump got pissed at Brazil having its own payment system without Visa/Mastercard network deleting billions in revenue from Visa/Mastercard

The problem major problem is already mentioned: Each EU country wanna have their own independent system. Nothing prevent the countries from doing that but it must talk within the same payment network so people in the Netherlands can buy from Italy using their own payment system.

Own payment system is different than payment network :)

Of course, what could go wrong!!

Unbelievable, a chance to make a whole new standard, new system, new everything, but yet we still have the need to tie it to ancient protocols, only to find later it’s broken by design and we start adding all sort of duct tape solutions to make it “secure”..

This is either a completely and entirely stupid move by some boomers living in the 80s, or maybe, it’s intentional to enforce something insecure like a phone number/GSM as a “national ID” to easily track citizens and force them to have a phone number linked to their real life, and I think it’s the second one, the same reason why many “secure” chatting apps still require a phone number.

It's also more convenient than giving out an opaque UUID to your friend to transfer you money or something similar.

The bigger problem I see with this is it being one more service locked exclusively to Android and iOS devices, but it's the same with most currently used banking apps anyways.

After you provide your gov ID

https://www.comparitech.com/blog/vpn-privacy/sim-card-regist...

So now this phone number is tied to your gov ID and bank account, amazing design of a single point of failure based on a broken protocol (GSM).

Not to mention that some of the alternatives are owned by a consortium of... European banks.

And the SIM registration requirement in nearly every EU country exists for 10 years now - in my case it was as simple as replying with code to operator's message because they had my personal information already for over a decade. There was a grace period after which unregistered SIM cards become dead - the requirement was dubious but you had to comply in order to call, text. There were "solutions" I've bumped on in depths of the Internet but neither felt serious nor safe.

I could get it without an ID and my (EU member) country is painted green/blue on those maps in your source. I always love it when people from abroad try to tell me how things work in my country, when they clearly have no idea.

Amex acceptance is lousy for a reason

Card and cash users alike.

> Well, either the US or China.”

> The host’s response — “I didn’t realise this” — captured the broader European blind spot.

People have been firing warning shorts for years. It is not a blind spot. It is just being ignored.

Not part of US not part of EU either.

what a losing proposition.

if it can be a card network with fraud protections that visa offer -- this will easily overtake Visa, Mastercard

Brazil with Pix have already proved this.

Not necessarily

If we can have visa and MasterCard while not being part of the US, we can potentially take part in whatever the EU creates

Terrible store of value(worse than bitcoin) Horrible International transaction fees(swift much worse than bitcoin) Most money laundering and criminal activities happen in the current banking system.

We rode on USA infra for too long. Europe is full of "managers".

When China and Russia have their own pay systems, why not EU?

As long as all the other cards still get acceptance, this seems like a great system.

> The Wero app can be installed on any mobile device or tablet running iOS 16 or later, or Android version 9 or later. We recommend updating your device to the latest version of its operating system for maximum performance, convenience and security.

> It is not possible to use Wero via a web browser or on a computer.

Your comment is of course downvoted

1. You first need to install an app (because you want to use tap to pay)

2. Then you need to download another app to authenticate the first app

3. But to set up the 2nd app you need to wait for an actual physical mail which contains a code.

4. Then you set up the 2nd app, but then again it asks for you to do a KYC using your Id Card.

5. Now you need to download another app to do the KYC using your Id, but it asks for another code which you receive by physical mail when you got your Id years ago, but you have no idea where that mail or code is, now you have to request for another code and wait like 2 weeks till you get a physical mail with that code....

.... and the story goes on.

I guess France and Germany are siblings in kafkaesque administrative shenanigans.

Why a subset of the EU and of Europe?

The fact that EU sees dependence on American tech in the same way as Russian oil now is saddening and telling.

Americans and American companies had it really good - our tech extracted money from the world, and they were mostly willing to pay for it. And it was an incredible advantage to the US.

But now, it seems that we are happily throwing all that away, for what benefit I do not yet see. Regardless of whether this effort succeeds, why stoke this fire at all?

I would say I hope Americans realize what they’ve done by making their own companies enemies of the world at large, but I’m not holding my breath for any sort of self reflection.

Though at least in Germany we have "girocards/EC-cards" that are not owned by Visa/Mastercard. Some banks are phasing them out in favor of a Visa/Mastercard debit card.

So maybe this is just an attempt to make Wero a bit stronger in comparison to PayPal. AFAIK Wero does not replace a credit card.

all of this infrastructure Europe claims to want to build will take many many years to realize, particularly at the relaxed European pace. trump will be out of office by the time the EU has held it's fifteenth planning meeting to issue it's first strongly worded letter of intent.

America was called an "enemy of Europe" (before the Greenland stuff) even though it was more generous towards Ukraine than a bunch of European countries, and essentially every country outside of Europe. Polls showed that China has higher approval than the US in Europe, despite the fact that China actively supplies war material to Russia. Again, this was before the Greenland stuff (I'm against that obviously).

There's no point in trying to please these people. They regard us as a vassal state. They're not joking when they say they think of Americans as idiots. We should've withdrawn from NATO a long time ago. Hopefully Europe's corporate boycotts will help to pass Massie's withdrawal bill.

It will also be interesting to see drug prices in Europe rise after the Europeans spent years making fun of the US for high drug prices. https://marginalrevolution.com/marginalrevolution/2026/02/tr...

The Europeans tend to reap what they sow in the US/Europe relationship.

https://en.wikipedia.org/wiki/NATO_bombing_of_Yugoslavia -- another offensive "humanitarian" action

By withdrawing from NATO and pulling our military bases out of Europe, it becomes more difficult for the US to "intervene" in the Middle East at the pleasure of Middle Eastern interests.

Furthermore, if Russia invades more countries in Europe, I don't want the US to "intervene" with yet another "humanitarian" operation.

We can slash the size of our military and spend that money at home on healthcare, debt reduction, etc.

and you said China actively supplies war material to Russia. but in early 2025, China’s top UAV export destinations were Hong Kong, the Netherlands, and the United States, https://www.airmobi.com/from-billion-dollar-orders-to-global... why Netherlands need so many UAV? That's why polls showed that China has higher approval than the US in Europe.

Furthermore, Europe has very little soft power in the US at this point. There's no region of the world I am less interested in helping. With every post I read from you guys, I understand more and more why my ancestors left that place. Think of it this way: We need to reallocate money away from our military, and towards our healthcare system which you guys are always making fun of. Does that help make my point clear?

As a user named raven12345 stated:

>Is there any doubt that a country that hasn't fought a war in decades is more popular than countries like the US and Russia, which are constantly at war?

We in the United States need to stop involving ourselves in so many wars. Plain and simple. You said it yourself.

>So why should they care about competition between China and the US elsewhere?

Where did I say that? I don't want the US to be competing with China. I'm an isolationist. I prefer a Swiss approach to foreign policy for the United States.

>That's why polls showed that China has higher approval than the US in Europe.

So we need to drop sanctions on Russia, like China has done, so that the Europeans will like us more?

"...companies — possibly with the tacit approval of customs authorities — have also engaged in classification fraud, concealing sensitive goods under misleading labels. In addition, some shipments are routed through third countries to disguise their final destination in Russia. By continuing to publish detailed customs data, Beijing openly signals its disregard for Western trade sanctions against Russia. But the data reveals only what China chooses to make visible — and it remains unclear what volume or categories of trade may lie beyond the published figures."

https://kinacentrum.se/en/publications/china-russia-trade-in...

"To help prevent a further deterioration of Russia’s economy and defense industrial base, Russia has leaned heavily on China. China-Russia trade reached nearly $250 billion in 2024, up from $190 billion in 2022.46 China has been Russia’s top trading partner since 2014, with its share of Russia’s foreign trade increasing from 11.3 percent in 2014 to 33.8 percent in 2024.47 In addition, Russia relies on oil exports to China, which now make up about 75 percent of China’s imports, compared to a pre-2022 average of between 60 and 65 percent.48

In the defense sector, China has significantly increased exports to Russia of “high-priority items,” a set of 50 dual-use goods that include computer chips, machine tools, radars, and sensors that Russia needs to sustain its war efforts.49 While Russia lacks the capacity to produce many of these goods in sufficient quantities, China’s massive manufacturing sector can produce a number of them at scale.50 Chinese exports helped Russia triple its production of Iskander-M ballistic missiles from 2023 to 2024, which Russia has used to pound Ukrainian cities.51 In addition, China accounted for 70 percent of Russia’s imports of ammonium perchlorate in 2024, an essential ingredient in ballistic missile fuel.52 China has also provided Russia with drone bodies, lithium batteries, and fiber-optic cables—the critical components for fiber-optic drones used in Ukraine, which can bypass electronic jamming.53"

https://www.csis.org/analysis/russias-grinding-war-ukraine

Contrast the $250 billion Russia/China bilateral trade figure, with the $146 million worth of drones which the Netherlands imported from China. Like comparing an apple to a grizzly bear.

$146 million is also fairly tiny compared with the $60 billion worth of weapons that Europe bought from the US over 2022-2024: https://www.iiss.org/online-analysis/military-balance/2024/1...

When you buy weapons from the US, it's a worrisome dependence on an evil warmonger. When you buy weapons from China, it's "yay we are buddies with China now". See why I've had enough of your "friendship"?

For years, Europeans have sharply criticizing the United States for sometimes partnering with authoritarian countries. It's fascinating to see the rapidity of your reversal: how eager you now are to partner with China, an authoritarian country which happily trades with Russia. It goes to show that this "don't partner with authoritarian countries" stuff is just disingenuous virtue signalling.

Unless you have already prescribed to the acceptance of big countries swallow the small ones at whim, it is not only our problem. Also Russia gaining control means often the USA loosing.

> Why don't you ask your new friend China for help?

Who said China is the friend of Europe? The USA has become a new unpredictable adversary, while China is an old enemy. Human nature is just to choose certainty over uncertainty even if that is actually worse.

> We need to reallocate money away from our military, and towards our healthcare system

I don't think EU countries have a problem with that. They rather complain, that you are currently allocating money to a military, that wants to attack EU states and to a para-military that attacks USA citizens.

> So we need to drop sanctions on Russia, like China has done, so that the Europeans will like us more?

It is that China is seen as evil anyway, so nobody expects them to sanction Russia for real, while we didn't saw the USA that way.

> For years, Europeans have sharply criticizing the United States for sometimes partnering with authoritarian countries.

You don't criticize enemies, you criticize friends. I think the criticism also was more that you create authoritarian countries, partnering was also done by European nations, that's called realpolitik.

The US is a big country. Why would it be affected by a problem of big countries swallowing smaller ones?

The Europeans always argue that the US only acts in its self-interest. But then when they explain why helping Europe is in the self-interest of the US, they always have the most nonsensical arguments.

>Also Russia gaining control means often the USA loosing.

I favor a policy of neutrality and world peace, not rivalry between major powers like the US and Russia.

>It is that China is seen as evil anyway, so nobody expects them to sanction Russia for real, while we didn't saw the USA that way.

Why is China more popular than the US in European opinion polls?

>You don't criticize enemies, you criticize friends.

That doesn't make any sense, you criticized Russia plenty. Furthermore, European "criticism" of the US is far too mean-spirited for it to be plausible that you are our friend. (That's been true for decades.)

>I think the criticism also was more that you create authoritarian countries, partnering was also done by European nations, that's called realpolitik.

Interesting how "realpolitik" can be used to explain European behavior but not American behavior.

It's always the same double bind. If we are involved, we're called imperialist. If not, we're called complicit. There's no way to win.

Because of less trading partners? Because supply chains exist? Because big evil empire is still better than bigger evil empire that is also a neighbor? Because treating problems when they are "small" is less resource-intensive then when they have grown? Because you have military-bases in these regions that you use to project power across the world? Sorry, but don't say you don't find them useful. If you wouldn't have a use for them, you wouldn't use your software power and money to maintain and them. Europe has long appeased the national interests of the USA as inheritance of the world war two, which like you say has also raised reluctant opinions.

> they always have the most nonsensical arguments.

Do you seriously think, that globalization can let you reap the world as a cash cow, but aggression, war and destruction in a not so far part of the world, even if it is no longer your ally, won't affect you?

> Why is China more popular than the US in European opinion polls?

I already addressed exactly that:

>> The USA has become a new unpredictable adversary, while China is an old enemy. Human nature is just to choose certainty over uncertainty even if that is actually worse.

It is just not known what the USA are going to do in the next 10 years. From slippery-slope to an open alliance with Russia to do a Polish-style division of Europe and America, over war with China to actually having midterms and a 180° turn in policy, all seems possible.

> That doesn't make any sense, you criticized Russia plenty.

While believing to have some power via financial ties. Now it's back to formal complaints and deadlines.

> European "criticism" of the US is far too mean-spirited for it to be plausible that you are our friend.

From the European viewpoint the criticism on the US administration is what would be also in the interest of the US populace. The US electorate of course begs to disagree, they elected Trump after all. Sorry, that protesting against expansion of corporate and state surveillance, influence of the military industry conglomerate and erosion of worker and environment regulation offends you personally. I fail to see how that is mean-spirited.

> That's been true for decades

The same criticism has existed for decades, but the official policy has stayed the same for a long time, namely that supporting "our" camp in world politics is worth compromising on international law, human rights and national security interest.

> Interesting how "realpolitik" can be used to explain European behavior but not American behavior.

It literally just used the word to explain American behaviour.

None of these arguments make much sense.

>Because treating problems when they are "small" is less resource-intensive then when they have grown?

I don't think it is a problem for us either way. No one is going to attack the US.

>Because you have military-bases in these regions that you use to project power across the world? Sorry, but don't say you don't find them useful. If you wouldn't have a use for them, you wouldn't use your software power and money to maintain and them.

The US has made many mistakes in its foreign policy. I've made my opinion clear on that. Just because we did something in the past does not make it a good idea.

>Europe has long appeased the national interests of the USA as inheritance of the world war two, which like you say has also raised reluctant opinions.

Well you'll be glad to stop then.

>Do you seriously think, that globalization can let you reap the world as a cash cow, but aggression, war and destruction in a not so far part of the world, even if it is no longer your ally, won't affect you?

Tell that to the Swiss.

American soldiers should not die due to European ineptitude. There were only 2.5 years between Pearl Harbor and D-Day. Russia invaded Ukraine almost 4 years ago. If you truly believed this was an existential threat, then you've had plenty of time to prepare.

>It is just not known what the USA are going to do in the next 10 years. From slippery-slope to an open alliance with Russia to do a Polish-style division of Europe and America, over war with China to actually having midterms and a 180° turn in policy, all seems possible.

How about you respect our ability to determine our own foreign policy, and take responsibility for your own issues? As I said, stop treating us like a vassal state and telling us you know what is best for us (as you do in your comments). I'm not the only one who notices you doing this: https://substack.com/home/post/p-158145261

Look at this argument I had the other day... a European spent a bunch of time condescending to me, and wasn't able to muster a single factual argument in favor of their position. This sort of thing is very typical in my discussions with Europeans: https://news.ycombinator.com/item?id=46742363

When Elon Musk endorses parties in Europe, Europeans complain he is interfering in their politics. The trouble is that Europeans have been doing the same in US politics for a heck of a lot longer. It's always the same patronizing and ignorant interference, based on a caricatured view of the US: https://www.noahpinion.blog/p/eurocope "Haha, Americans are dumb. Haha, Americans die in school shootings. Haha, the American healthcare system sucks." All along, we've been deterring Russia for Europeans, and now as a result, Russia is working to destabilize the US (according to another commenter in this thread). I'm sick of it.

Think of it this way. I want out of NATO, so as to reduce the influence of the evil "military industry conglomerate". Just like you yourself said, we need to reduce its influence -- which means reducing our military size and commitments. Get it? I'm just taking your arguments to their logical conclusion.

> US foreign policy analysts think that every issue is the next WW2

If "US foreign policy analysts" would actually think that these situations might lead to the next WW2, then you wouldn't counter them with destabilizing countries, that leads to the rise of extreme parties and then treating them with ignorance. Because THAT is exactly how WW2 happened.

> If we are involved, we're called imperialist

Deploying the military is not the only way to get involved.

> It's always the same double bind. If we are involved, we're called imperialist. If not, we're called complicit. There's no way to win.

If other countries say that has bad consequences, you deploy the military, if they say we need your help here, you turn the blind eye. I mean you are a sovereign country and can do what you like, but you do it, because your administration thinks that is a good idea, not because all the other countries would tell you to. You frame it like other countries called for action and you did them and now they complain. No, they told you they won't like that, and you did it either way.

Nope. Just the opposite. The reason the US did regime changes during the Cold War was because we were paranoid that communism would affect us. We need to be less paranoid.

>Deploying the military is not the only way to get involved.

Doesn't matter, we're called imperialist however we choose to get involved. Ever heard the term "neocolonialism"?

>If other countries say that has bad consequences, you deploy the military, if they say we need your help here, you turn the blind eye.

Even when US military action is requested or approved of by people in the country, we're still called imperialists. Consider the war in Vietnam. The South Vietnamese were attacked. We came to their aid for some time. They kept fighting after we left. Yet this was still described as "neocolonialist" activity on our part. That's how our actions are always described.

I was more thinking of "post" Cold War interventions.

> Doesn't matter, we're called imperialist however we choose to get involved. Ever heard the term "neocolonialism"?

Yes. The US isn't alone in that situation. The EU is described as neocolonialist in the same way. Personally I think that is stupid and we shouldn't have let us be influenced by that. Now Europe stopped being "neocolonialist" and the Chinese has taken over that role in Africa. Now it's much worse both for us (EU) and for Africa. Great.

> Consider the war in Vietnam.

Honestly I wasn't alive and don't know the public opinion of that time. I basically only know it from history class. The rough sentiment is that the French messed up and the US has payed for it. It's true, that some actions in the war are portrayed as bad, most famously Agent Orange, but I think the war in total isn't blamed on the US.

> That's how our actions are always described.

Reading the other thread you linked, I think you have a worse view of the public opinion of the US then it actually is.

> I favor a policy of neutrality and world peace, not rivalry between major powers like the US and Russia.

> Russia should use its special services within the borders of the United States and Canada to fuel instability and separatism against neoliberal globalist Western hegemony, such as, for instance, provoke "Afro-American racists" to create severe backlash against the rotten political state of affairs in the current present-day system of the United States and Canada. Russia should "introduce geopolitical disorder into internal American activity, encouraging all kinds of separatism and ethnic, social, and racial conflicts, actively supporting all dissident movements – extremist, racist, and sectarian groups, thus destabilizing internal political processes in the U.S. It would also make sense simultaneously to support isolationist tendencies in American politics".

In other words, they want an endless line of Donald Trumps to ruin your country and turn it into a banana republic so that you wouldn't have the energy to pay attention to Russia stomping over the rest of the world.

Why would any American voluntarily choose this fate?

None of this would've happened if we had avoided imperialism post-WW2.

"mopsi" stated how you going isolationist and stuck in domestic struggles, is following Russias plan. So no, the current state of the US results in you stopping to

> "contain" Russia and protect Europe through NATO.

So this is what the EU complains about and tries to tell you: you follow Russians plan and that can't be in your best interest. (Not that the EU would be free from such interests either.) Do you think Russia would leave you alone when there plan succeeded? That would be the biggest success of Russian policy since 1945. When they can get you from the major world power to being a isolationist country with domestic struggles, why would they stop?

> None of this would've happened if we had avoided imperialism post-WW2.

I think you need to define terms here. What exactly counts as "imperialism post-WW2" and what not? I mean the arms race let to the collapse of the soviet union, so I guess until to the 90s it went pretty good for the countries part of the "First World".

If you wouldn't have stayed in Europe after WW2, the USSR would have reached to the Atlantic. And no not just in 1945, they also tried that in the 50s and continued to want that. Not sure, if you already know, but Putin was in prison in Germany in the 90s for trying to topple the German government and his goal was to expand the "Soviet/Russian" empire to the Atlantic. He was already ~40 and has served in the KGB before, so I guess he hasn't changed his opinion since.

The current deteriorating state of the US is the result of departure from the previously held values and forms of cooperation. Nothing illustrates this better than the US president openly threatening the sovereignty of Canada and Denmark while accepting massive bribes from Arab sheikhs and calling genocidal dictators like Putin his "friends". This is the wet dream of people who want to see the US fail.

Why would any American want to hit the gas pedal and accelerate even further down this road?

Last August US threatened tariffs on Brazil over their Pix system. One of the reasons given was that people using Pix instead of credit cards deprived Visa and Mastercard of fees.

Just a correction: the US imposed those tariffs. Threatened too, I guess, but the Orange Man did more than that.

It's not as much about replacing Visa/Mastercard, as it is about plastic card technology becoming obsolete, and the duopoly failing to react to the market because of corporate inertia. Had they created a modern online payment system, Wero would never take off.

As an european, I'm for all the european tech stack funding projects going on, but I'm also glad we move on these other issues without waiting forever.

One not-so-fun fact is that when the US sanctions anyone, their ability to transfer and use money via Visa etc. is taken away. In the modern world, being cut away from even using your debit card is a huge, massive hassle.

It is one of the many different ways being sanctioned makes life more difficult. I can't imagine the US being too keen on giving up those powers.

You'd add a lot of technical complexity, especially if you need this to be instant. You'd loose the ability to effectively fight fraud, and because of this get a huge target on your back attracting all sorts of unwanted behavior.

On the other hand, you'd gain... nothing? Especially since consumers cannot be expected to run their own blockchain stack, they'd need to fully trust their banks and intermediaries anyhow.

Money would go directly bank-to-bank, nothing in the middle.

If the government is going to act irrationally and (through visa/mc) prevent legitimate transactions then people will just deal with fraud.

Even if Europeans agree with the DLsite ban they see the writing on the wall for European eCommerce sites.

The article briefly touches this point but dismisses it saying wero and the digital euro complement each other, but doesn't go into detail on how. I see no point in a privately run digital currency when we can have a public one. I guess whichever has good privacy, reliability, ease of use and speed will win.

(but it probably won't ever happen, because banks are lobbying against it with FUD campaigns, they feel like it threatens their existence)

Wero is something completely different. It allows consumers to easily pay merchants, mostly online. The digital euro is not a payment network in the same sense as Visa, Mastercard, iDEAL and others.

https://www.ecb.europa.eu/euro/digital_euro/faqs/html/ecb.fa...

It says they'll have offline transactions, if they have that, then you can probably make those "offline" transactions from Kms away from the receiver. We'll see how things evolve, I'm still not convinced that wero will have any use once the digital euro arrives.

Or, an easy way for vendors or car rental agencies to block a set amount when you rent a car.

However, all of these things can be built and I hope Wero gets the time to grow into a full alternative to US-based payment systems.

Not because I want them to fail, but because this market can use a bit of competition and new ideas.

Probably merchants like Netflix would also love recurring payment functionality. Let's just hope they'll make them cancelable this yime.

Earnest question: is the EU really Visa and Mastercard's most profitable market? I would have expected it to be the US, both by customer volume numbers and in terms of regulatory environment (i.e. the US allowing payment processors to take a larger cut).

Smartcards with PINs were ubiquitous much much sooner (it being a French idea did not help for US market penetration), which means today the magnetic stripe on our cards is little more than decoration. Seriously, I'm 29 and I've yet to see a single magstripe payment here (while it was daily when I went to the US).

Also, we pretty much only have debit cards (don't know why, but don't know why I would want a credit card). This is even less risk for both the network and the merchant and the bank, reducing issues for all links in the chain.

Or the fact that Europe has 100M extra people in it, and a lot of countries seldom use cash nowadays.

I disagree. In Portugal, MB Way arrived, allowing people to use their phone to send money to each other, or pay in terminals, and it was widely adopted. People want ease of use and low fees, not to keep their credit cards.

With this being said, the Digital Euro has more potential.

Living in the Netherlands iDeal is perfect for online shopping, but once the money is gone there is no way to get it back.

With Visa/Mastercard there is a level of protection available which leaves the door open to get your money back if you are being scammed.

I believe Wero is going to implement this as well, so time will tell but I think any move to break the duopoly of Visa/Mastercard is good for consumers.

In Asia you can pay with Alipay in most countries. In South America you can pay QR codes via Mercado Pago (for example).

Or at least make this new system interoperable with the more established players worldwide without the need for a Visa/Mastercard.

That's exactly the problem. Several actors have won the market of their country, but only of their country.

Will Trump be enough to make the europeans realize that they need to work together, and that an italian win is just as good as a german win?

For someone from france, sure.

For both italians and germans, it matters who wins (and i'm not making a pun here).

I agree with you

However that specific example somehow feels off and déjà vu

wow, so not even all of the European Union, not even all Eurozone countries, hmm

I get their SEPA system but do they really not have a functioning credit network between consumers and merchants?

The digital euro could be a good candidate here and it also aspires to have cash-like privacy features. It's also mentioned in the article as separate and hopefully non overlapping product.

I think it's absolutely amazing that "crypto" (from bitcoins to shitcoins) have turned out to be no more useful as a currency than chips from the local casino. This has damaged their ability to function as a simple currency that can be used to pay for goods and services. And they have damaged the reputation of the whole distributed ledger technology to the point where, in 2026, banks aren't even considering implementing a closed circuit inter-bank distributed ledger as a way to send euro from one bank account to another. If the digital currency in this closed system was actual euro, there would be no reason to speculate on its value and turn the whole thing into a circus.

I'm sure I'm missing something (a lot actually)

NASDAQ (NYC) currently runs on software/systems built and maintained by Stockholm-based developers. NASDAQ merged with Swedish OMX in 2008, founded as Optionsmäklarna OM AB in the 80s.

Developing countries have mostly leapfrogged to total contactless payments.

In South Aast Asia, you typically scan a QR code and approve a payment from your own phone. Far less fraud as a result. Nobody is able to touch your card, you don't have one.

Europe likely identified they better make the jump.

There are benefits to non-QR based payment systems, such as not wanting to pull out your phone, open an app, scan a QR and approve to make a payment that takes me 2 seconds with regular contactless payments.

Physical cards are also a nice fallback to have in cases of running out of battery, theft, etc.

We have progressively absorbed single function items into a mobile computer.

Watch, notepad, calendar, phone, flashlight, camera, dictionary, encyclopedia, etc.

The issue with declaring single function items as obsolete is that it removes redundancy and really sets us all up for an increasingly more critical single point of failure in our pocket.

Who returns your money to you if you purchased something on mail order with this, and it turned out to be fraud?

Debit or ATM cards are different. They pull money directly from your account and can exist independently of Visa and Mastercard. For example, some credit unions still issue ATM only debit cards that are not part of the Visa or Mastercard networks.

I've paid numerous time using the swiss counterpart, Twint, in small shops. For some like the farm I used to buy vegetables to it was their only supported payment besides cash because they deemed the card systems too expensive.

The same way chinese tourists can already pay with alipay in many retatail outlets in europe, you can already pay with such european systems on Aliexpress. More are probably comming.

Wero are not in the business of issuing cards, though obviously they could get into that business - just like UnionPay did in China. I suspect there would be a lot of inertia there, as card payment fees are capped in Europe anyway.

Granted, the FAQ entry is rather light in details:

https://support.wero-wallet.eu/hc/en-us/articles/39413057671...

Neither are visa/MC for the most part. Mostly debit. ;) this isn’t really about the card anyway but the network behind it.

This is likely to be similar to the existing European payment systems just wider in scope. There are a bunch already it’s just fragmented and country specific. Sepa wero ideal girocard crates bancaires

When did banks actually make that switch?

It must be relatively recent, because I remember not that long ago my credit union ATM card was not part of Mastercard. Now I have a new one and it suddenly has a Mastercard logo.

even better, its not public.

This depends highly on what countries and banks are involved.

If I (as a Swede) want to send money to my german friend, I have to use Revolut or Wise since going through my bank is an enormous hassle and involves higher fees.

And it's not secure or anonymous at all. At some point you need to buy crypto or sell crypto, or buy some goods with crypto, and at that point you can be easily identified. Happened so many times.

Even here in Russia, under all US sanctions, only a few use crypto. It's so inconvenient that even under pressure of US sanctions it hadn't become more popular.

Regarding anonimity when exchanging, yes. But you can make the same point about cash. You are identified when withdrawing, and identified when depositing. You cannot be identified when cash changes owners, and the same holds true for lightning payments. So if anonimity is the same, lightning is still to be considered superior as it works also for online payments while cash is bound to physical means of payments.

and you think the EU would want that?

It's free, their tech is great and their fx rates are more than fair.

Short-term negative-sum transactionalists are governing the US. Even if November stabilises things somewhat, the cat is probably out of the bag.

Trust comes on foot, but leaves on horseback. _That_ is why a well-integrated EU-based payment system is needed.

There are examples of other co-branded national payment systems out there (troy + Discover comes to mind).

If a European payment system (with cards, at a store) is to exist, then visa/mc will still want a piece of the pie by at least playing along to remain as a co-brand and taking their cuts from international payments.

So sorry, we do definitely get what this entails :)

Why would they continue?

>If you wouldn't have stayed in Europe after WW2, the USSR would have reached to the Atlantic. And no not just in 1945, they also tried that in the 50s and continued to want that. Not sure, if you already know, but Putin was in prison in Germany in the 90s for trying to topple the German government and his goal was to expand the "Soviet/Russian" empire to the Atlantic. He was already ~40 and has served in the KGB before, so I guess he hasn't changed his opinion since.

Interesting. So the US saved Europe, you say. Yet we get nothing but complaints, mockery, and condescension from Europeans. You mock us for the same military-industrial complex which saved your butts. Wonder why we aren't interested in saving Europe again?

Because they like to increase their influence and territorial control and already did the hard part? Granted the USA becoming like Iran or Venezuela today seems a bit of a stretch. I honestly lack the imagination how a USA in ten years, that hasn't had elections that actually affect things, serves the best leader of all time and is a major ally of Russia looks like. There will also be so much other territorial changes in that scenario.

> Interesting. So the US saved Europe, you say. Yet we get nothing but complaints, mockery, and condescension from Europeans.

I don't think you get much mockery about the US cold war policy *in Europe*. Granted these people exist, but they also often do sit in the same party that merged with the ruling party of the GDR.

> You mock us for the same military-industrial complex which saved your butts.

I think a military industry propped up in war times by the government, and the resulting military complex having subverted civil rights and politicians are different situations. A military that is conjured by the people makes a country stronger, large "dead capital" in weapons and industry starting to control the government becomes dangerous.

> Wonder why we aren't interested in saving Europe again?

To some point yeah. I'm not going to say the EU hasn't made bad decisions in the last 30 years. I don't see it that black an white, so e.g. "So the US saved Europe, you say." I would say the US in alliance with West-European nations did save Europe, the Morgenthau plan wouldn't have helped against the USSR either. But my main argument for this discussion is, when the USA go isolationist now, it first messes up a lot of other things in the process and second the same will repeat that happened in the 1940s, there will be the need for the USA to intervene, because it affects their bottom line, and the situation will be much worse, and it causes much more loss (of human life).

This is essentially the same that process the EU just went through. It did "nothing" in 2014, because that is not NATO and we don't want to get involved in a war, and now it became worse. (I think our "we did get involved too much" is Yugoslavia, to some point participation in wars with the US and of course WW2.) Now we did get involved, because the next border will be a NATO and EU border. Sure, we can say it won't happen, Russia is not THAT strong, but the next decision would be to either get the EU in a complete war against Russia, or to give up on the territorial integrity of EU states. And we don't want to face that.

If we continue the discussion, I think it stops to make sense to treat both the US and the EU as single entities, because in both there are parties that have been arguing for one policy and for others.

They didn't just switch. They purchased Discover.

edit: added the "just"

Also to say, cash remains. That's more radical and effective as a fall back than a card which one can lose. When abroad I remember the anxiety of losing my wallet when abroad. With a phone, it's actually less problematic to walk into a shop, get the cheapest android in there and set up all my banking on it. Half a day of a holiday wasted, that's an acceptable inconvenience given the risk. Losing a card, not really.

> Also to say, cash remains. That's more radical

?!

> and effective as a fall back than a card which one can lose.

Cash loss is a thing, actually. Plus cash is more attractive for theft.

These are not open or interchangeable standard, they aren't interested in that. They want our valuable transactional data, and location when those are made.

QR codes are a standard. It allows any bank to issue funds. It's a wire transfer. Transfer are a standard. Any bank can adopt it. Typically a bank adopts it..it doesn't require a specific device or partnership for merchant, nor the payer.

It also offers the ability to transfer funds remotely. In that sense it is more so contact "less" than the proximity handshake that contactless payments do, which is somewhat proprietary.

You can save a QR code, make a payment later. QR codes also are more intuitive because they represent an identity. An electronic device that can be swapped, tempered with, is unhelpful to help figure out a fraud or who we are actually paying until the handshake happens.

More importantly they don't incur a hidden fee for either the payer or merchant. Because it's a transfer. Not a transfer disguised as card payment.

A QR code scan keep the payer in control. Merchant presents an amount to pay, payer initiates the transactions, approves, and gets a confirmation. Can use bank A, or Y, or even a bank in another country, so long as it supports QR scan and a fast wire so that the merchant can be assured the transfer is well received.

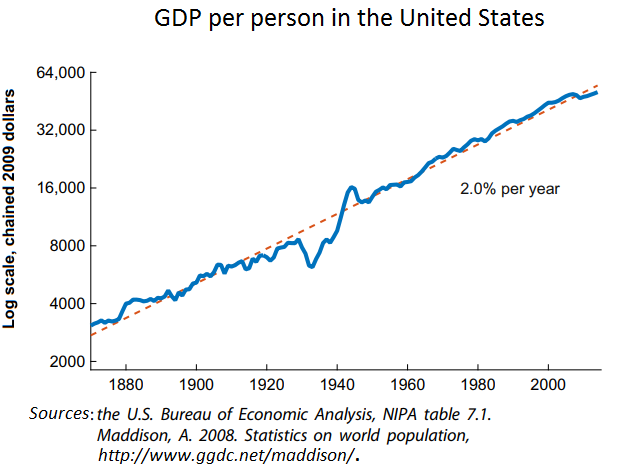

https://upload.wikimedia.org/wikipedia/commons/0/01/GDP_per_...

You yourself just explained how Russia saw us as a threat and destabilized our politics, which lead to the current situation. We would have been better off if NATO was never formed.

If you believe I'm a Trump supporter then you're misunderstanding my position.

> The US prosperity trend has been the same before and after WW2:

> You yourself just explained how Russia saw us as a threat and destabilized our politics, which lead to the current situation. We would have been better off if NATO was never formed.

Other sources disagree: https://ourworldindata.org/grapher/daily-median-income?tab=l...

But it doesn't matter--you're arguing that prosperity for the average US worker began stagnating about 20 years after the formation of NATO. That's basically an anti-NATO argument, from the US perspective.

>Russia fundamentally wants to see you fail and take your place in the world.

My goal is to abandon our place in the world and be like the Swiss. I don't want to destabilize yet another country (Russia in this case). We're gonna have to live with Russia whether we like it or not.

Russia has made major leaps in destabilizing your politics since we (the EU too) believed we won the cold war and stopped treating the Russian empire and allies (which China definitely was, now it's more equal or the opposite) as a threat. The USA also has a superiority complex, like most European nations also had, which certainly isn't helping now.

> If you believe I'm a Trump supporter then you're misunderstanding my position.

You said the USA going isolationist is going to solve problems, which granted isn't as extreme as the Trump foreign policy, i.e. it won't fuel the worsening of the current situation, but it isn't going the improve it either.

… banks saw big, no, BIG $$$ and lost their minds. The transition was rather swift: between the very late 2000's and approximately 2015 (give or take a few years), the transition had been complete. Credit cards became a massively profitable and booming business for the banks, with all sorts of loyalty programmes and bonuses (at consumers’ expense, of course, as the banks also jacked up interest rates on revolving credits). Note that all of this took place before national governments stepped in to regulate the transaction fees.

This coincided with the growing allergy of Western governments to owning any critical infrastructure (including payment networks) and the rising trend of outsourcing as much as possible to the private sector. As it is easy to imagine, it did not take long for the national banks already being in bed with Visa/MC to convince their respective national governments to stop investments in maintenance and enhancement of domestic payment networks and delegate the payment processing to the cartel: «they can do it better than you do».

… all of which has led us to where we are right now. Technically, national payments are still alive, but they are more in the contained mode of operation and not in active use or development.

Europeans use these dispute protections much less, so Visa/Mastercard are mostly seen as expensive pass-throughs.

And in Europe, when people hear Mastercard or Visa, they just associate the name with refused payments at points of sale depending on the luck they had with the merchant, or the foreign country, etc.

I do agree that in this case, picking MC/VISA is not really important. When I changed banks a few years ago, it so happened that I switched from a Visa to a Mastercard. Nothing changed save for the logo on the card.

But that might be one reason why business ideas from the US do not always translate well to Europe, and vice versa.

As to how, in the financial term: we europeans don't really have the credit culture the US has. Having a credit is something very last resort, especially for "trivial" stuff (e.g. christmas shopping, to keep your example). Most europeans will have one or two credits tops: real estate loan, and sometimes car loan. Companies (mostly US) start offering payments spread over multiple months, but it does not really have a high penetration (at least in France), being in small useless debts is something we avoid like the plague.

And how do we have enough money in the bank? We just shop after payday, not after. Or, for most people, we keep a somewhat constant amount in the daily account. It's just another way of managing your own money.

Also, such terminals often use multi-carrier data plans that can use the best carrier available, while your own phone is stuck with one of the options (of course, you always have the worst one).

When you go to your local restaurant, do groceries you are paying a few percentage in tax for using you card.

Platforms online already act as escrow anyway. PayPal, Stripe, act as escrow..yes they take a percentage, but that's more granted for these cases.

PayPal and Stripe are the payment processors who are taxing the card usage and acting as escrow. The technology part of transactions is with Visa and MasterCard. Who will do that part for free if they are not to be involved? What would be the benefit of separating escrow and processing, and how would it realistically be done?

Irregardless of what the economic data actually says, why is this to be blamed on the NATO? I don't see the causal relation. If there was indeed something in the 1970s then I would default to blame the oil crisis.

> My goal is to abandon our place in the world and be like the Swiss.

They were directly in between the other nations in WW2 and capturing them made no sense for the others. They are also pretty small and lie in naturally protected mountains. I doubt the USA can become that, they are just too large.

Also the Swiss just gave that up partially. How much is currently under dispute. https://en.wikipedia.org/wiki/Swiss_neutrality#Russian_invas...

> We're gonna have to live with Russia whether we like it or not.

Yeah, I guess the US is in the privileged position that they can make that decision baring cyber attacks and domestic destabilizing.

> Other sources disagree

> But it doesn't matter--you're arguing that prosperity for the average US worker began stagnating about 20 years after the formation of NATO. That's basically an anti-NATO argument, from the US perspective.

> My goal is to abandon our place in the world and be like the Swiss. I don't want to destabilize yet another country (Russia in this case). We're gonna have to live with Russia whether we like it or not.

As for Russia, you have the luxury of shaping the kind of Russia you live with. Is it the Russia that enslaved half of Europe and is using their brains to build a massive stockpile of nuclear missiles to blackmail you while you dig shelters in your backyard out of fear for your life, or is it a different, more peaceful Russia that has abandoned imperialism like Germany was forced to? Isolationism is a fool's errand. You can very well pretend that the war in Ukraine doesn't affect you, but consider that the nuclear missiles Russians tried to set up on Cuba were built in Ukraine. Would you rather have Ukrainians living under Russian boot and building nuclear missiles to burn down American cities, or have them building rocket engines in support of NASA space explorations programs like they did in the same Soviet-era nuclear missile factories in the early 2000s? It's not a difficult choice.

Most countries in the world don't have a choice and have to deal with whatever the life throws at them. You do have choice. Use it wisely.

I don't see why they would be, generally speaking.

"it’s very difficult to look at a country where the typical person lives in a larger house, is more likely to own a car, eats more meat, and uses more electricity than people in other rich countries, and to conclude that this is “a poor society”." https://www.noahpinion.blog/p/no-the-us-is-not-a-poor-societ...

>In monetary terms, Americans consume more health services than anyone else, yet have fallen behind in life expectancy

US life expectancy has little to do with our healthcare system. See https://xcancel.com/jburnmurdoch/status/1641799742228144130#...

>The prosperity of the average worker did not begin to stagnate when NATO was formed, but indeed decades later

My claim is simply that NATO is not key to our prosperity. Post-NATO stagnation, insofar as it exists, is quite compatible with that claim.

>Switzerland is entirely surrounded by the EU, and its economic prosperity depends on access to the European Common Market.

None of the objections in this paragraph would apply to a more geopolitically neutral US. The US economy is large and relatively self-sufficient. Imports and exports are a relatively small fraction of our GDP.

>nuclear missiles Russians tried to set up on Cuba

...after we set up missiles in Turkey...

The Cuban missile crisis demonstrates the danger of American belligerence, and the importance of us being more peaceful, less paranoid, and more neutral.

Can't we have cards for this? In Spain, for example, to use Bizum, you need either an Android/iOS smartphone (and for the Android case, as you use it from your bank's app, it would typically require some Google security assurances - so no Huawei phones allowed, for example) or logging into your bank's website and use Bizum from there, only if your bank allows you to use Bizum via web. And it's not very practical or convenient to do that when you're in a store and want to pay, in contrast to swiping your credit card.

So while I see very convenient gaining some sovereignty from American companies for these payments, I think we're losing it when we will need devices controlled by other American companies in order to use the new system.

What about being required to carry a your-own-government-controlled tracking device?

Because the US or Chine government can't harm me in Europe via the data they collect from me, But the EU authorities can if they want to, so naturally I fear them more if they were the ones hoovering my data.

What are the odds they're using this on-shore tech grab to implement their own domestic version of China's social credit score system, to easily get data on their own citizens who commit "wrong-think", without having to through the effort to twist the arm of US entities every time they want to do that?

Food for thought, but I do think we're living the last years of online anonymity, it's inevitable.

One only needs a few looks at what the EU Commission has been doing lately to see that if left unchecked their plan is a UK-like total surveillance state.

The usual first victims are sex workers, not political minorities.

Attestation in on itself isn't unwarranted which (to me) is an important security measure. Attestation as commonly implemented on Android via Play Integrity (the way banking apps are known to do) is restrictive, sure: https://grapheneos.org/articles/attestation-compatibility-gu... / https://archive.is/snGEu

The article starts with Wero right off the bat, which a pan-European rebrand and continuation of the Dutch Ideal. The Dutch have been using Ideal everywhere, and you usually use that to pay online. It redirects you to your bank to acknowledge the transaction, and most bank have auth methods where a smartphone is optional. Most often used for sure, but optional, and you can complete the transaction with a hardware reader and your debit card as well.

The only exception are the neobanks like Bunq, which actually are smartphone-only. That one in particular is great if you appreciate the CEO and staff keeping a personal eye on your transactions (no kidding).

They sold their transaction platform as a service to Apple Pay. And funneled all your transaction data to palantir.

Financial networks are side channels for intelligence gathering. And that makes the folks doing them outside of your nation an adversary.

With the US choosing to become an enemy of western democracy in Europe, the need for more investment in building trusted core infrastructure is inevitable.

Certainly none of this is ever simple. But this is just a microcosm of a much larger shift across many industries in Europe and we as tech nerds should be mindful of the tectonic shifts that are happening currently. The capital investments occurring have serious long term implications for us all.

My point being, if these payment systems start becoming more interconnected and join within a standard, I wouldn't be surprised if we eventually saw Bizum cards around here, Wero cards in other places, and many more.

At least that's my take on it. Of course there's still a long way to go, such as developing the system, banks adopting it, businesses adopting it, then customers (which would probably take years, many people wouldn't bother switching at least until their current card expires)

[1] https://www.bbva.com/es/es/empresas/bbva-primer-banco-en-esp...

I don't know about Huawei, but actually most (all?) of the banking apps in Spain should work on a non-Google-certified Android builds. There's an community list tracking GrapheneOS compatibility at https://privsec.dev/posts/android/banking-applications-compa... and all of them currently appear supported just fine.

https://www.androidauthority.com/why-i-use-grapheneos-on-pix...

> Police in Spain have reportedly started profiling people based on their phones; specifically, and surprisingly, those carrying Google Pixel devices. Law enforcement officials in Catalonia say they associate Pixels with crime because drug traffickers are increasingly turning to these phones. But it’s not Google’s secure Titan M2 chip that has criminals favoring the Pixel — instead, it’s GrapheneOS, a privacy-focused alternative to the default Pixel OS.

EDIT: Previously on HN: https://news.ycombinator.com/item?id=44473694

But isn't the promise of Apple Pay that you never expose your real credit card # to the merchant? So they can't track you? I know Walmart in Canada really resisted Apple Pay for a few years because it would mean no more ability to track people by their payment methods.

What's an extra layer of surveillance? Why accept the "credit and debit" surveillance middlemen but not the google/apple middlenmen?

What the world needs are "cash cards". Something equivalent to cash not tied to your identity that you can use in the real and virtual world.

I simply do not understand why governments or the private sector do not provide such options.

How exactly are you doing that? with 3D Secure online credit card transactions now require confirmation in the mobile app (or via OTP sent by SMS, but this is being phased out, as it is insecure)

Likewise, in Germany we can have SEPA for most stuff.

And in Greece there is Viva.

Problem is getting something that actually works across all European countries.

While we may make most of our payments within EU, basically everyone still occasionally pays for something outside of EU, either online or when they travel. This means if the new thing only works in EU, every European will still need and have a MasterCard/Visa even if they use it less often than before.

This is still a massive amount of leverage - MC/Visa still have the ability to block payments made from EU citizens/companies to outside.

https://en.wikipedia.org/wiki/Unified_Payments_Interface

It sounds a lot like what they're discussing.

I would also hope so, that is the entire point. The reason they are scrambling right now is because Starlink just shut off all of Russia. Because Starlink was so cheap and easy (and stable for the last 4 years of the war), a lot of people in Russia stopped using any other form of internet access. And while all of Europe is happy to see Russia go away, they are concerned that the same can be done to them at a whim by any number of American companies. So they are trying to quickly create alternatives to anything American including software providers like Microsoft 360.

As for credit cards, it is not as if there is something intrinsically American in credit card processing. They can just as easily create a new system that uses the same protocols as Visa and Mastercard.

Having your entire economy dependent on a company you don't control in a country you don't control was considered acceptable for as long as a concept of "allies" existed. That is not the world we are living in right now.

What you're saying is just plain false. No one has ever used Starlink in Russia. It doesn't even work here. It never did. Russian troops were using Starlink on Ukrainian territory, that's what was shut off.

They're the same bright minds that ensured no alternatives could naturally come out of the European market trough relentless bureaucratic central planning. I have zero hopes of a good outcome

What are you smoking ..err.. any source to your claim ? (Which is between bizarre and just plain wrong).

What are you talking about? Starlink never worked in russia. It worked in Ukraine, and it was shutdown in Ukraine by using a white list for which any Ukrainian can easily apply.

The goal was to shutdown Starlink usage by russian drones in Ukraine and by anyone on the occupied Ukrainian territories.

Pasting this ddg-ai thing but I think its called UPI 123PAY

UPI 123PAY allows users to make digital payments using feature phones without needing a smartphone or internet connection. Users can set up a UPI ID by dialing *99# and can make payments through methods like IVR calls, missed calls, or sound-based technology.

By the way, since you wondered, it seems to be

> built around the digital wallet Wero

and wikipedia says its a mobile payments method. I hope not. I hope it's rather an interface/spec.

(On a side note, I also hope individual countries of EU ensure that those spec leaves an ability for them to continue internally or even externally if rest of the EU decide to cut someone off or so.)

Wero is the implementation. I think it makes sense to provide a turnkey solution to all participating banks, so that we don't have 100+ versions of the same app.

Countries that don't want to trust EPI (or simply outside the Eurozone) are able to take the same path as Bizum in Spain, and make their domestic solution interoperate with EPI instead of replacing it.

Are you aware of any banks that don’t require you to use their Android/iOS app to use PIX? I’ve had accesss to maybe a dozen banks and none had that ability. Sometimes you get via web, but needs their app’s 2FA to log in.

I completely agree. Sadly UPI is now almost completely dependant on platform integrity ( google and apple).

Even if it does, Google won't be taking a cut from it.

Also, it's then much easier to provide a mobile web version, or something else.

My country's internal system also sells a bracelet for contactless payments, and there are obviously payment cards.

Once there's a mandatory standard, it's much more likely competition will show up. EU wide SWIFT, direct debits, instant transfers, all show this.

Cards will have a slow demise over the next 10 years but it's coming whether we like it or not.

Like to log into e-banking services over here we either have phone apps, or a code calculator device that can be used instead of those: https://www.seb.lv/en/private/daily-banking/tools-and-online...

Seems like common sense to me, the same how I have a wallet on my phone but still carry cards for payments just in case.

No, these companies keep themselves in power not because they've solved such a difficult problem that nobody else can, but because they have a moat which they protect.

Time to do away with these foreign entities.

We've already got a strong payment processing brand with Interac, it's used daily for millions of debit transactions, and supports all the features you'd expect (in Canada) from a payment card (tap, chip&pin). There's also the MasterCard Debit and Visa Debit branding which seem to bridge debit transactions to the MasterCard and Visa networks. And there's already Interac-capable terminals basically everywhere that Visa and MC are accepted.

My thought is that Interac should launch a credit card brand called "Interac Credit". The actual credit would be via the banks, just like it is with Visa and MC. Interac already has the relationships with merchants and banks to make this happen, and it has the mindshare with consumers to make it successful.

Wero is like a monolith, while EMPSA is more like mobile phone roaming. If I would bet, I would bet on EMPSA.

https://en.wikipedia.org/wiki/European_Mobile_Payment_System...

Point being that with a cheap alternative, it's actually much more convenient now to use a Visa or Mastercard especially with tap to pay because with competition being so high, the diversity means people allow all payments.

https://x.com/moo9000/status/2006304163404128289

The difference this time is that Digital Euro is forced by ECB and control (and deposits) are taken away from banks.

> The core problem has always been fragmentation. Each EU country developed its own domestic payment solution — Bizum in Spain, iDEAL in the Netherlands, Payconiq in Belgium, Girocard in Germany — but none could work across borders. A Belgian consumer buying from a Dutch retailer still needed Visa or Mastercard. National pride and competing banking interests repeatedly sabotaged attempts at unification.

> The network effect compounds the challenge. Merchants accept Visa and Mastercard because consumers carry them. Consumers carry them because merchants accept them. Breaking that loop requires either regulatory force or a critical mass of users large enough to make merchants care — which is precisely what the EuroPA deal attempts to deliver by connecting existing national user bases rather than building from scratch.

It's now been about a month since a White House deputy chief of staff for policy and homeland security advisor openly talked about/advocated for taking Greenland by force. POTUS was vague for a while.

Northern European nations sent like a hundred military officers to Greenland. POTUS then threatened those nations with, wait for it, tariffs.

Then the markets crashed and Rutte/Nato provided a face-saving de-escalation path.

Their site claims that it can only be used on iOS or Android: https://support.wero-wallet.eu/hc/en-us/articles/25599074240...

Also:

> It is not possible to use Wero via a web browser or on a computer.

This seems an even worse situation than carrying around a Maestro (mastercard) with me.

In what way specifically? Android and iOS are just the OS the banking apps that implement Wero happen to run on. There is nothing stopping them from releasing a Linux app. Or a web app.

“Breakup” seems a bit exaggerated considering the % of payment volume which might switch to the new system.

Is it really just PayPal left offering a sane online payment service?

---

From https://support.wero-wallet.eu/hc/en-us/articles/25599074240...:

> It is not possible to use Wero via a web browser or on a computer.

But now i think of it… how does Visa and MC do it? Cuz i dont have a username or phone nber with them (i know they have my number). But i havent switched my number, so maybe if i did, i would have an issue?

I can send money ONLY to my contacts. It doesn’t allow to type in phone number, one needs to create a contact.

I feel like Europe is just doomed. The stupidity is endless here.

It didn’t work for the amount we needed (over 15k).

Biggest banks here refused to support Apple Pay and worked hard on legislations to open NFC access. Now we can pay with no fees to Visa/Mastercard or Apple even from our phones.

Instead, we are getting a digital euro, a fully dystopian abomination.

But I'm sure there are plenty of villains and idiots that will try (and succeed) in diluting those principles and will get some dystopian (trace everything) version of that.

Even Polish banks discourage using debit cards directly and just switch to Blik.

Lost card? There's no card, so doesn't apply. ATM skimmers? Nope, I think all ATM support Blik, so can't sniff anything. Want to send money to a friend? Instant mobile-friendly transfer. It's even possible that the family can pull the cash out from the ATM from your account when you're in a different city if you'll give out the code.

Just the transaction processing fees going to VISA and Mastercard now would probably pay that back within a few years. Also, we're talking about all or almost-all European countries. So it doesn't sound like that much.

> Low interchange fees under EU regulation make profitability difficult.

Mandating that businesses which accept US credit cards must accept the European payment card would take care of that. Actually, maybe that's not necessary, it's probably enough to mandate that companies making card processing tech which supports US credit cards must also include support for this card; and businesses would just get it with their next system upgrade / terminal replacement or something.

> Consumer habits are deeply entrenched

I 'like' how people are described as "consumers", as though every payment is for consumption.

Anyway, habits are not that deeply entrenched. Didn't people adopt those country-level payment cards? Don't people occasionally change credit cards? It's not even a change of tech, it's just yet another card.

> and neither Visa nor Mastercard will sit idle while Europe tries to dismantle their most profitable market.

Now this may be a significant factor... they could influence politicians, tech solutions makers (with sweetheart deals if they don't support the new payment tech, or whatever), they can get the US government to make some kind of threat (we've already seen the threat to invade Greenland). So, yeah, there's that.

Item two is convenience. All these systems are "faster wire transfers". I don't really see the point of them when you can already do instant IBAN or even phone number based transfers.

What they do not have is a line of credit backing them. Got to make sure you have money in "the particular system your merchant accepts". Also at least in eastern europe credit cards come with the possibility to pay in a few installments with zero interest (paid for by the merchant of course, so not everyone does that). This is gone in the new system.

What they also do not have is the fraud protection of a credit card. You may be able to revert a transaction but the money is gone from your account and it will take a long time to see it back.

On the other hand it's harder to spend money you do not have so perhaps the EU is trying to make its citizens more financially responsible? :)

* Cards are convenient. No need to go get cash, no change at each transaction to manage carrying around. * Cards give a discount in the form of "cash back". (As mentioned elsewhere, this really just inflates the cost of everything for everyone, but I might as well claw it back.) * I don't actually go "into debt". I pay off my card (automatically!) every month, and incur no interest charges. I use it like a slightly deferred debit card with benefits.

The last bullet being significant to your point: I don't "spend money on [a] loan".

Of course it only works to your advantage if you pay your credit cards in full every month.

Card terminals here in Poland usually accept BLIK payments

It is also very popular payment method in e-commerce

In Czech Republic we have QR payments. They're ok, but could be more streamlined...

Let them focus on offering a payment system, and let others focus on their thing.

In particular, I heard this through Mallen Baker at https://www.youtube.com/watch?v=7ACzkuSFzT4

It's an app that uses NFC or, if needed, reads a QR code and does a web request (i.e. needs internet).

Neither Google nor Apple will block that, or take a cut; and it's already available in multiple markets.

This is about taking stuff that already works in one or two countries, design a similar system that works across countries, and mandate that all banks under ECB supervision implement it.

Google keeps self-sabotaging Android Pay. They lacked market power so cellular carriers blocked it hoping to advance their own payment ecosystem (ISIS). Google changes the payment brand every few years, and fragments it into two separate apps or combines them. It's rather like their messaging strategy.

So I don't think distribution is a problem. Of course companies would prefer to save the cost, and they also prefer that you use their applications, but I just don't think it's more convenient for the end user. Taking a card with you is not a big deal while having to use a mobile application or approved device limits your freedom to choose which smartphone you want to use or how to use it.

It makes sense to build upon modern SEPA payment rails and focus on mobile wallets. Europe has always been on the forefront (Swish, Vipps, ...) and we have entire generations of consumers who barely if ever use plastic cards.

Might as well make it to the brain while we are at it. Safe when one is brain dead or unconscious. What say?

But 99.99% of the time won't be the implementation of such interfaces, but monitoring and security.