YC Demo Day Session 2(techcrunch.com) |

YC Demo Day Session 2(techcrunch.com) |

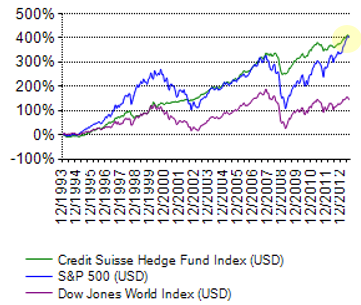

Hedge Funds on average do not outperform market indices such as S&P 500. I'm curious as to whether this was TechCrunch's take on the problem, or the startup's?

Buffet (S&P500) is leading against hedge funds on the aforementioned long bet: http://fortune.com/2014/02/05/buffett-widens-lead-in-1-milli...

Disclaimer: I am on Buffet's side on this long bet. Management fees are the devil. I am all-in for low-fee index funds.

Venture capital is different because it is both correlated with market returns and the average fund significantly underperforms the market,[1] so getting good returns in venture capital is pretty much a question of getting allocations in the top 20 funds, which are persistently the best. They have the best returns in part because they have the best reputations and thus access to the deals that provide the highest returns (top entrepreneurs would take Andreesen Horowitz's money over money from Unknown Partners on the same terms).

1: http://www.kauffman.org/~/media/kauffman_org/research%20repo...

http://fortune.com/2014/02/05/buffett-widens-lead-in-1-milli...

How do you suppose one tell which hedge fund will do better and which won't beforehand? Past performance? We know that's not a good indicator. If you can tell which hedge funds will do better in the future, you probably can tell which stocks will do better, and then why not just got it yourself without giving someone else 2 and 20?

We agree that S&P500 and hedge funds have different risk factors.

The point is that S&P500 is a lot less riskier and with better returns than an average hedge fund.

From what I recall, one of the big problems that any reactor project has is that the reaction has a tendency to destroy the reaction chamber. Not just the heat, but the neutron radiation can completely screw up the reaction chamber walls, which then need replacing. It's one of the reasons the ITER project is so large, to make it relatively robust in the face of such destructive power. I also remember reading a while back that the force from the electromagnets in the ITER project is sufficient to launch the entire reaction chamber off the ground, something like 5000 tons...

Having said that, I think it's cool that they're attempting it and I think that fusion projects have been grossly underfunded in the past. The reason why it's always 30 years away is because they're always cutting the funding!

I'd love to be proven wrong on this, but I imagine they'll have unexpected escalating costs surrounding the actual building of a working durable reactor and the company will die before it gets off the ground.

Just of late I came across this graph which says something similar: http://i.imgur.com/JyUZDe2.jpg

One of our major advantages is that we're a bit more ambitious about deploys and we try not to limit you to a certain format: you can deploy any type of application on Flynn, not just web apps, but regular applications and services like databases, mail servers and so on. We then let you connect all of these together via service discovery. Meaning that instead of limiting you to a plugin system, Flynn allows you to write your own "plugins" that behave just like regular apps.

I have observed that hospitals invariably manage to saddle me with ridiculous "processing fees" and suchlike and add around $100 or more to my expected charges every time I visit them. I usually just pay up to avoid the nuisance of dealing with administrators who cannot seem to be able to communicate over email, and possible damage to my credit if I try to challenge it. I strongly suspect this is the case for a lot of middle-class Americans.

I'd gladly pay the same amount to Fixed to act as an intermediary between me and said 70s-era administrators, if only to let them know that someone is looking carefully at their exorbitant charges, and possibly even contesting them.

What am I missing? Thoughts?

Also, it certainly doesn't mean they'll put Kash out of business if they do (and if the Kash team succeeds). For example, I don't expect Amazon Local Register to put Square out of business.

However, I clearly see the many benefits for the retailer. They are saving money on transaction fees, avoid charge backs (maybe?), get paid more quickly, and is free for businesses charging under $100k.

I think in the back of my mind when I posted my previous comment was the classic chicken-and-the egg problem. Lots of benefits for retailers, but only if customers use it. Possible benefits for customers, but only if retailers accept it. I think that many of the other larger existing players in this space already have most of the infrastructure in place (eg, Square) and have brand recognition to boot. So, I see a very large uphill battle for Kash in this space with their business model. However, as you point out, it isn't necessarily a zero sum game and Kash could exist along side competitors. It will be interesting to see if they can differentiate themselves in some way and/or execute better in some way.

To be clear, Sliced is open only to accredited investors and has a minimum investment of $20,000.

And here's the best part: http://ftalphaville.ft.com/files/2014/08/Screen-shot-2014-08...

It's clearly not the case that I cannot select a set of hedge funds that is less risky than the S&P500. Fixed income funds, for example are much less risky (ignoring for argument's sake some details like inflation risk). I don't know if the "average" hedge fund is more or less risky than the S&P500. Depends how you define average. But no one is investing in the average, you couldn't do so even if you wanted to.

And as for clearly better funds like A16Z and YC now, there have many numerous that have held that crown before. Fees and fund expansion have resulted in worse results -- allowing newer players like A16Z and YC to take off.

My argument is that I don't think it's clear who'll beat the broad market (for their asset class) once the fees are taken out. I suppose we disagree about the value of high-fee managed funds (whether VC, PE, Hedge, etc.). That's fine.

Anyway, enough digression from the discussion on hand.

Good luck to the founders in making their value proposition clear. I am sure there are lots of people want to invest in hedge funds but don't have the funds to invest directly. They will find this appealing.

The point is they are not open to investment once you have historical evidence that they are "good".

> Funds also sometimes charge less than the maximum they can get away with for various reasons.

The only reason I can think of is to increase investment. But that will happen even for minimal excess return.

> Moreover, you are ignoring the very real excess profits that are made on the way to this hypothetical equilibrium. Berkshire Hathaway shares aren't going to make you rich if you buy them today, but I'm guessing the people who bought them in 1970 don't care.

Obviously there are excess returns the question is if they can be reliably identified before hand and are accessible.

Are you invested in hedge funds? Which ones do you think are good now?

{kind=link}

{kind=link}

{kind=link}